50% Additional Expense Deductions for Corporate Entities

On 20 January 2020, the Thai Official Gazette No. 137 introduced the Thailand Tax Royal Decree No.690 (issued under the Revenue Code regarding Revenue Exemption B.E. 2553) to give corporate entities a 50% additional expense deduction for investments made in new machinery. Corporate entities which operate the business of leasing and investing in machinery for the purpose of leasing will not qualify for this additional deduction.

The deduction is only applicable to investments in machinery made from 1 September 2019 to 31 May 2020. The Machinery Registration Act B.E. 2514 (1971) defines machinery as anything which consists of a part that either generates, converts or delivers energy; however, this definition does not include vehicles registered under the Motor Vehicle Act B.E. 2522 (1979).

The Machinery Must

1. Not be previously used and should be ready for use by 31 December 2020;

2. Be subject to wear and tear, and these expenses can be deducted under section 65 bis (2) of the Revenue Code;

3. Be located in the Kingdom of Thailand;

4. Not have received tax privileges under the Royal Decree issued under the Revenue Code, whether in whole or in part;

5. Not be utilized in a business which is exempt from Corporate Income Tax under the laws on: investment promotion (Investment Promotion Act B.E. 2520 as amended by Act No.2 B.E. 2534 and Act No 3 B.E. 2544); on increasing the country’s competitiveness for target industry (Act to Enhance the Competitiveness of Targeted Industries B.E. 2560); or the law on special development zones in the eastern region (Eastern Special Development Zone Act B.E. 2561 (2018)).

Preparation Requirements

Companies or juristic partnerships entitled to the income tax exemption under the Royal Decree are required to:

✓ Establish investment projects and payment plans; and

✓ Notify the Director-General of the Revenue Department (the Director General) in accordance with the rules and conditions to be prescribed by the Director General.

Failure to comply with the above procedures and requirements will result in the withdrawal of the tax benefit with effect from the first accounting period it was used, and tax returns from the relevant accounting period will need to be re-filed. If the machinery is sold, damaged or no longer exists, the tax benefit will end in the accounting period in which any of these events occur and there will be no need to re-compute the tax benefit.

Updated Eligibility Criteria

Further criteria and conditions for this tax benefit have been elaborated upon under the Notification of the Director-General of the Revenue Department No. 366, dated 13 February 2020.

✓ A contract, hiring order, purchase order or any other agreement of similar nature made between September 1, 2019 and May 31, 2020, is a prerequisite to support the investment which has been made in the new machinery.

✓ It is required that the machinery be included in the fixed asset register for the corporate entities.

✓ Should corporate entities utilize this tax benefit, they must prepare an investment project and payment plan by 31 May 2020 using the prescribed form on the Revenue Department website. Furthermore, such entities must prepare a report that lists the specific machinery relevant to the tax benefit (and provide supporting documents), as well as other information required in the Notification.

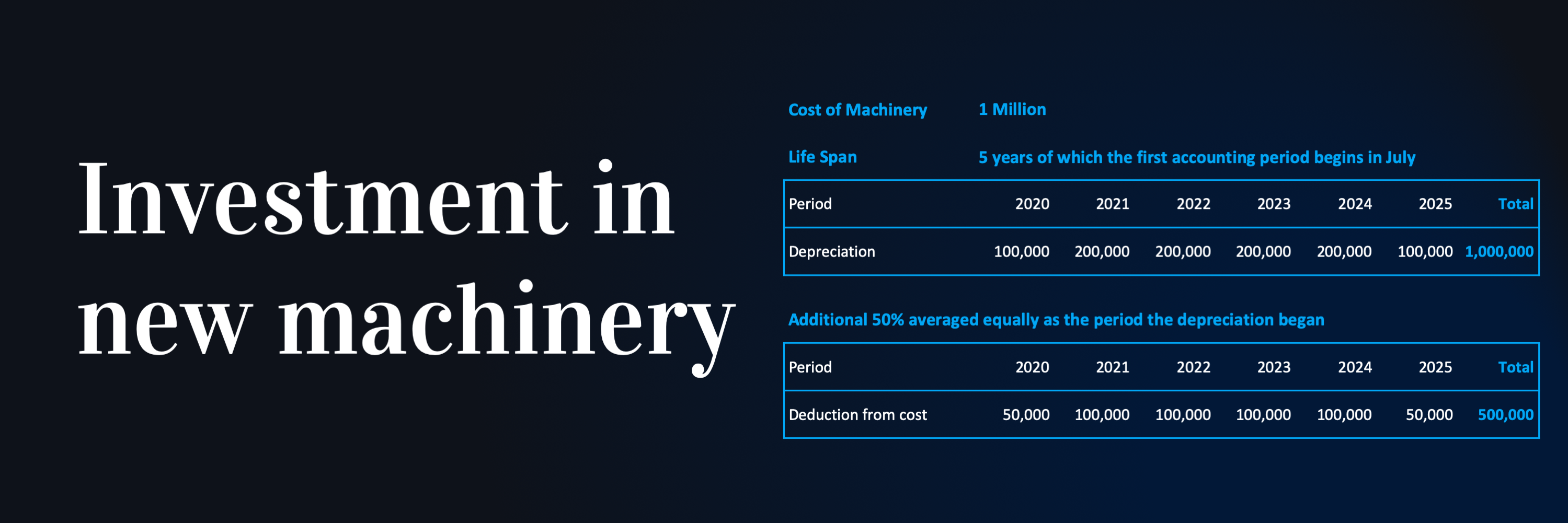

✓ The 50% additional deduction will be averaged equally over each accounting period for 5 consecutive accounting periods, commencing in the same accounting period as that in which the depreciation began.