What is blockchain?

A blockchain can be described as a spreadsheet of transactions, or an electronic ledger, which is distributed among a network of computers. Blockchain transactions record aspects such as amount, date and time, and unique digital signature. As transactions occur without a central or intermediary authority, this promotes a more secure and transparent process while reducing intermediary costs, times and transaction fees. Using blockchain technology for trade finance means faster and more transparent cross-border trade and reduced reliance on paper and manual processes.

The three main pillars of blockchains are:

1. It is decentralized, therefore money can be transferred directly between parties without going through a bank,

2. It is transparent, meaning all transactions can be seen by anyone; and

3. It cannot be edited or tampered with, as the digital ledger is spread across the network of computers.

What is trade finance?

Trade finance is a process whereby a financial institution grants a credit facility in order to ensure security over the transfer of goods.

As a hypothetical example, Company A in Thailand wishes to import goods from company B in Japan. The importer is hesitant to issue payment before receiving assurance that the goods will arrive and the exporter is hesitant to send the goods without securing payment for them. To address this deadlock, the importer’s bank issues a letter of credit to the exporter through the latter’s bank, ensuring that payment will be made once relevant documents (such as bills of lading) are provided. This protects both the importer and exporter as the respective banks handle each party’s funds.

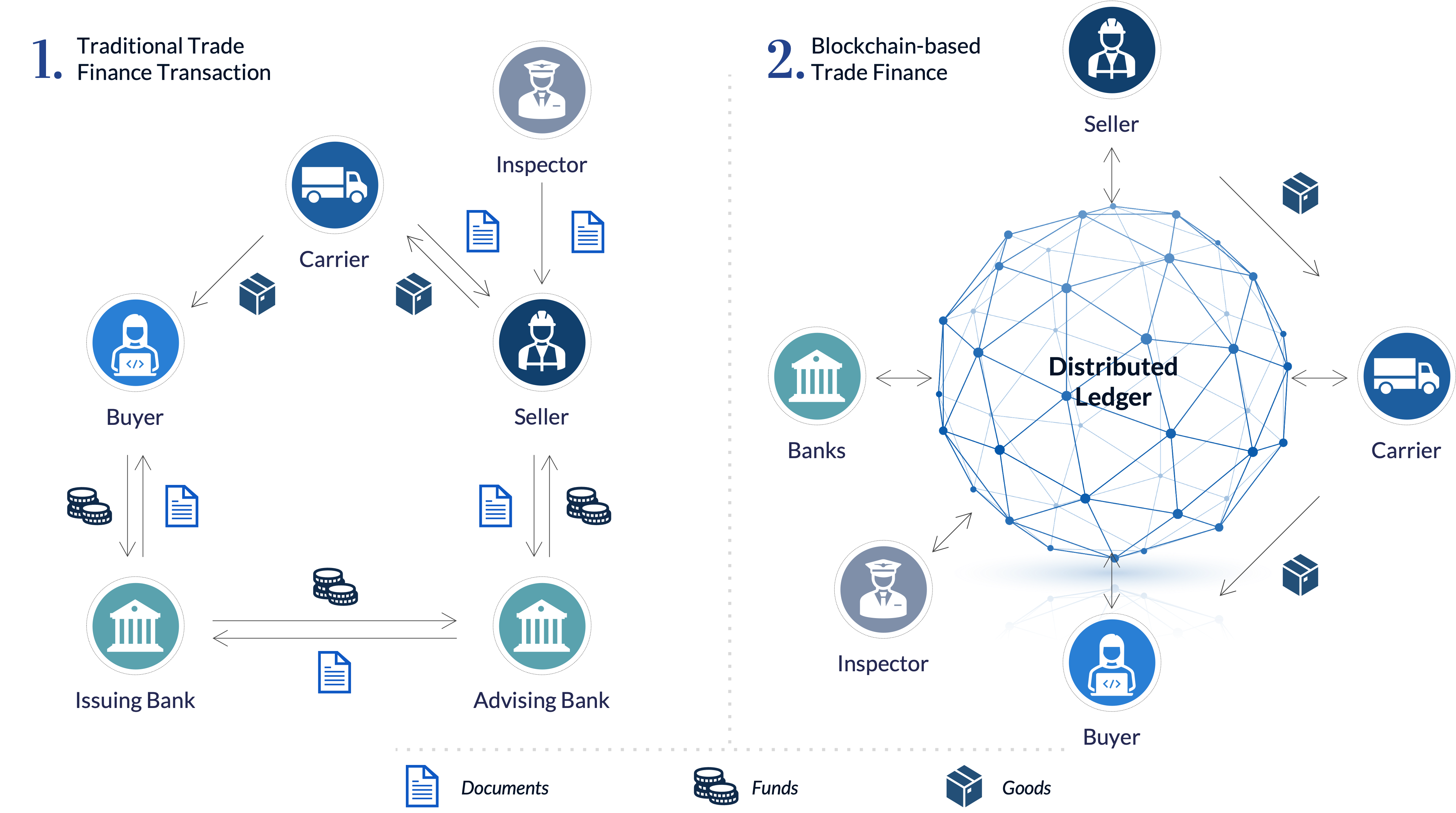

Figure 1. Traditional Trade Finance Transaction vs Blockchain-based Trade Finance.

How does blockchain work?

A blockchain-based transaction is initiated by creating a ‘block’ (i.e. a list of records) that is verified by a number of computers and added to a chain. If one record is falsified, the entire chain becomes invalid. Blockchain technology, which is used for cryptocurrencies, is also used to store smart contracts.

As an illustration, when a credit card-holder purchases an item on a specific website, a credit card issuer would charge a fee for processing the transaction. However, the introduction of a blockchain would mean that the purchased item becomes the ‘block’ that is added to the blockchain in a unique and immutable record.

A smart contract (or cryptocontract) is a computer protocol created to verify and enforce underlying contractual obligations, such as the transfer of digital currencies or assets between parties if certain conditions are met. Smart contracts can be used to transfer money or property without an intermediary, thus making banks and financial institutions redundant. Implementing these types of contracts will play a major role in streamlining commercial transactions.

Ways in which trade finance can be reshaped by blockchain

Cross-border trade transactions have been underpinned by trade finance instruments for centuries and have been characterized by very slow-paced change. Globally, trade finance transactions are governed by the Rules of the International Chamber of Commerce (primarily, the ICC publications UCP 600, ISP 98 and URDG 758) and are hosted by the SWIFT Platform, which settles and records transactions. Despite being the world’s major platform for domestic as well cross-border payments worldwide, the SWIFT process has inefficiencies. In 2018, the Financial Times observed that SWIFT transfers frequently “pass through multiple banks before reaching their final destination, making them time-consuming, costly and lacking transparency on how much money will arrive at the other end”. In light of the shortcomings of existing payments infrastructure, blockchain technology would appear to be a much more efficient option.

Trade finance transaction procedures can be improved upon by blockchain in a number of ways. Currently, cross-border trade processes are subject to the following features which may present limitations:

✓ Manual processes used by the issuing bank (the importer’s bank) to examine sales contracts and import documents, analyze discrepancies, and provide financials to the exporter’s bank or correspondent bank can take time and be subject to human error.

✓ Invoice factoring requested by exporters who could present their invoices to multiple banks, thus obtaining financial leverage results in an increased risk profile in the event of default on delivery of goods.

✓ Delayed timeline resulting from the involvement of a multitude of financial intermediaries, each having their own compliance policies and internal processes to execute payments and/or issue/confirm lines of credit.

✓ Delayed payments resulting from multiple financial intermediaries seeking to verify that the documents presented comply with the terms of the documentary credit or the guarantee. This process may be rather lengthy, depending on the number of intermediaries in the correspondent banking chain.

✓ Manual Customer Due Diligence must be conducted by financial institutions, including Know Your Customer (KYC) review, Anti-Money Laundering (AML) checks and Financial Crime Compliance (FCC) evaluation.

✓ Multiple communication channels, means and formats are commonly used for trade finance, with underlying documents being presented either electronically or in paper format. This exposes businesses and banks alike to miscommunication and fraud.

✓ Duplicate documents can be presented to banks, which may result in processing the same transaction twice or more, and difficulties in identifying whether any financial institution has already underwritten (financed and/or guaranteed) a trade.

✓ Tampering with financial records may occur when the communication channel that is used is not authenticated or protected against unauthorized access. As a consequence, records may be manipulated, duplicated or falsified.

The foregoing represents some risks that financial intermediaries face on a daily basis. Blockchain technology has the potential to mitigate those risks or, in the best-case scenario, eliminate them completely. Blockchain could revolutionize trade finance in the following ways:

Figure 2. Ways in which trade finance can be reshaped by blockchain.

✓ Blockchain technology increases efficiency, as transactions are conducted directly between parties without intermediaries. Import/export documents can be accessed by all parties, and can be reviewed and approved in real time, thus eliminating errors and delays.

✓ Real-time access to trade documents ensures that the shipment of goods is initiated in a shorter timeframe, reducing time and costs of documentary as well as customs compliance.

✓ The risk of duplicate documents, such as invoices and bills of lading, is eliminated in as much as documents can be tracked.

✓ Enhanced transparency ensures compliance with current KYC/AML policies and regulations, facilitating the work of bankers, lawyers and law enforcement officers.

✓ Transactions can be easily traced, facilitating audit processes. This minimizes fraudulent activities as transactions are recorded in a transparent and sequential manner. A detailed analysis of past transactions would assist in conducting a risk assessment for future trades.

✓ In terms of security, transactions are individually verified through complex cryptography to ensure their authenticity.

✓ Collaboration is enhanced as transacting entities can share trade finance-related data with each other.

✓ Autonomy is increased as the introduction of smart contracts removes any reliance on a correspondent bank and payment of transaction fees.

Limitations in implementing blockchain technology

✓ Legal and regulatory frameworks may not yet be conducive to address the specific features of blockchain technology; for example, some countries only recognize negotiable instruments if they are on paper and signed. In addition, the anonymity of the unique identifier may render certain contracts difficult to enforce. Furthermore, as blockchains are not rooted in a specific location, questions arise relating to territoriality and applicable jurisdiction.

✓ Widespread application of blockchain technologies and automation of many manual processes will render certain jobs in the trade financing sector redundant, reducing employment rates and possibly creating detrimental associated economic impacts.

✓ The lack of standardization slows down the implementation of the blockchain technology owing to the high number of Distributive Ledger Technology (DLT) platforms. In addition, as consensus is required across networks, the system performance becomes slower.

✓ The system is still subject to human error as data entry is still carried out by relevant parties.

✓ There are data protection and privacy concerns, as transaction flows can be used to identify parties.