What is transfer pricing?

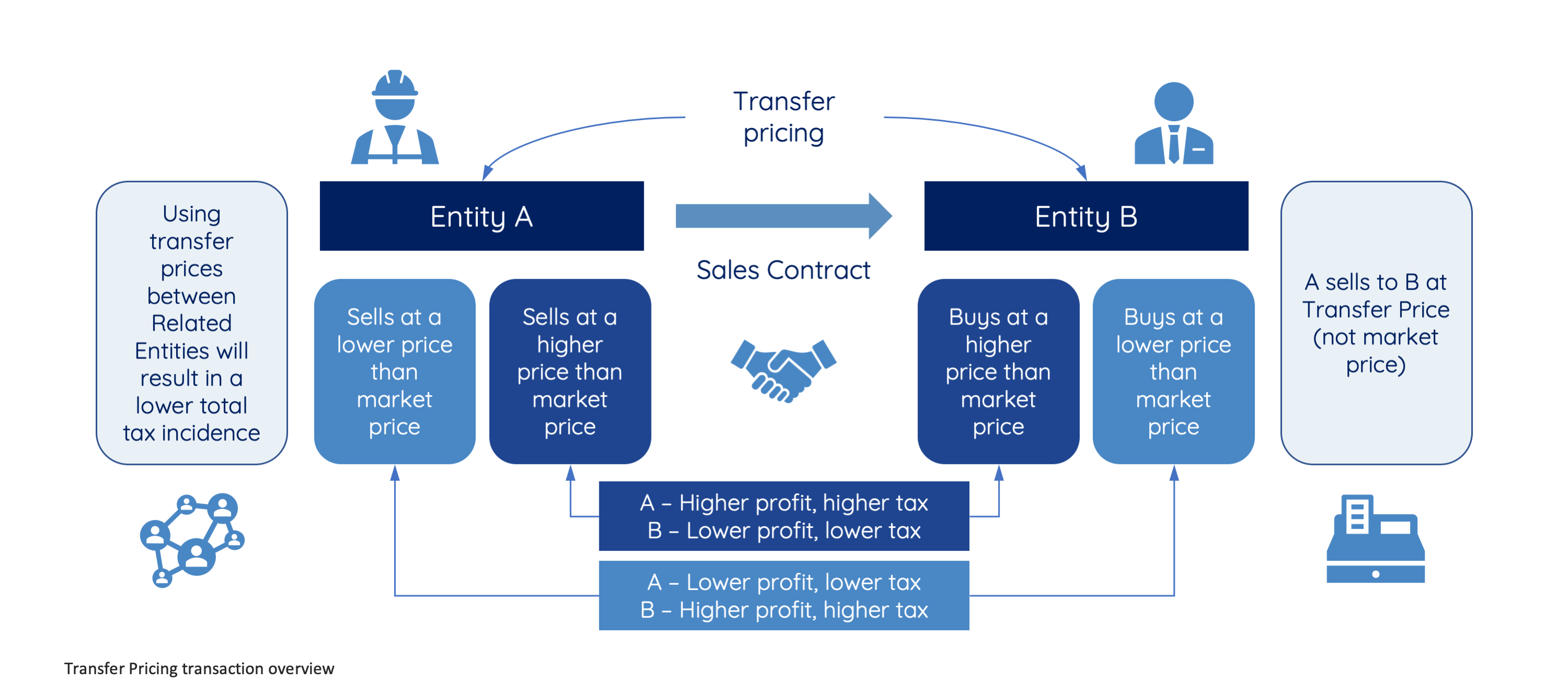

Transfer pricing determines the market price or tax valuation for cross-border or domestic transactions between related entities.

According to section 71 bis (2) a ‘related entity’ means an entity (or a shareholder or partner of an entity) that holds directly or indirectly a minimum of 50% of the total share capital of another entity. A ‘related entity’ is also defined to include, an entity that is related to another by way of capital, management, or power to control, and that cannot perform independently from the other entity.

The market price (or the arm’s length principle/price) is the fee which independent contracting parties would charge in a commercial manner for the same types of property or service provided, on the date in which the transaction is made.

What law governs transfer pricing in Thailand?

The Revenue Code Amendment Act (No.47) B.E. 2561 (2018) entered into force on 1 January 2019. This amendment was designed to bring the legal framework into compliance with international standards on how market price is determined, and to reduce opportunities for tax evasion between (legally) related entities within an enterprise.

The first filing date for a transfer pricing disclosure form, which should be part of an annual tax return, is 30 May 2020 for the fiscal year ending 31 December 2019. Certain provisions of transfer pricing will become applicable to accounting periods commencing on or after January 1, 2019.

KEY PROVISIONS

Which businesses are affected?

Section 71 ter (1) requires any business with an annual turnover of THB 200 million or more and that does not meet prescribed exemption conditions, to file a report showing the nature of transactions between related entities in each accounting period, submitted with their annual corporate income tax returns. This is required regardless of whether or not the relationship exists throughout the entire accounting period, and whether or not the related parties had inter-company transactions throughout the year.

Required documentation

Transfer pricing documentation needs to be prepared before or at the time of entering the related entity transactions. The Revenue Department therefore requires the relevant documents to be submitted within 60 days of a request (or within a further extended period of 120 days where the required notification has been made to the tax authority).

A tax officer may request the related company to submit transaction-related records within 5 years from the date of submitting the transfer pricing disclosure form.

According to Section 71 bis (1), if a tax officer is of the opinion that a taxpayer transacted with a related entity under different commercial and financial conditions than those which normally apply, a primary adjustment may be made on the entity’s assessable income and allowable deductions. Any double taxation agreements entered into by Thailand with another country will be taken into consideration.

Impact on Customs

As taxpayers are required to submit a transfer pricing disclosure form, the Thai Customs Department (TCD) will be able to scrutinize importers transactions and any customs valuation issues may be subject to inspection. For example, if the declared customs value on an import differs from the cost incurred on purchasing goods, the TCD may assess the related party’s transactions to determine accuracy of the declaration. Any importer that is found to have provided false information in this regard may be liable for duty evasion in accordance with section 243 of the Customs Act B.E 2560 (2017). This offence carries a penalty of imprisonment for a period not exceeding 10 years and a fine ranging from between 50% and 400% of the customs duty shortfall.

Tax Refunds

Section 71 bis (3) allows a taxpayer to claim a refund if the assessable income or deductions had been adjusted. These adjustments do not affect the Value Added Tax (VAT) applicable to the taxpayer. Generally, a refund may be claimed within three years from the submission date of tax returns, however, should the original submission date expire, and the taxpayer has already been notified of a transfer pricing adjustment, a request may be made 60 days from the date of obtaining the tax assessment letter.

Penalty Imposition

Section 35 ter illustrates that should a taxpayer submit incorrect or incomplete information without reasonable explanation, a penalty not exceeding THB 200,000 will be imposed. It should be noted that this is not a fixed amount, and each case will be determined on its merits. Taxpayers may be exempt from such penalties provided the required (accurate) documentation is submitted on time.

How We Can Help

As international trade and cross-border transactions are on the rise, so are requests for sound transfer pricing strategies that pass scrutiny by tax authorities. MPG’s team of experts in transfer pricing assists clients in complying with Thailand’s regulatory framework. Our team is well-equipped to conduct risk assessments, evaluate transactions, draft master files and ensure that the correct documentation is submitted to the appropriate authorities. Our services include planning and designing strategies, intelligence gathering, analysis, report production as well as preparing and submitting all relevant documents to tax authorities and regulatory bodies.