The internationalization of companies’ activities has led to the prevalence of cross-border intragroup transactions among related companies. In serving the overall interests of the firm, firm leaders have sought to reduce the parent company’s costs and aggregate taxes payable, notwithstanding that such a move may not necessarily be in the best interests of the individual entity.

What is transfer pricing?

Despite the lack of economic basis, related companies may engage in cross-border transactions for the purposes of tax optimization. However, they remain criticized by governments who often deem these transactions to be abusive, depriving the country of tax revenue from a company which imposes domestic economic burdens through its operations. This has led to the rise of transfer pricing rules which prevent such abuse of intracompany deals, while ensuring fair play and reasonable prices between related companies. Ultimately, these rules ensure that companies do not involve low-tax jurisdictions in their transactions merely for tax avoidance purposes, and that profits are taxed where economic value is created, and real underlying economic activities are performed.

In essence, transfer pricing determines the price of goods and services that are transferred to a related entity. In this regard, related entities are defined under Section 13(16) of the Income Tax Act (“ITA”) as those which (a) have direct or indirect control over one another, or (b) fall under the common control of another entity, in a direct or indirect manner.

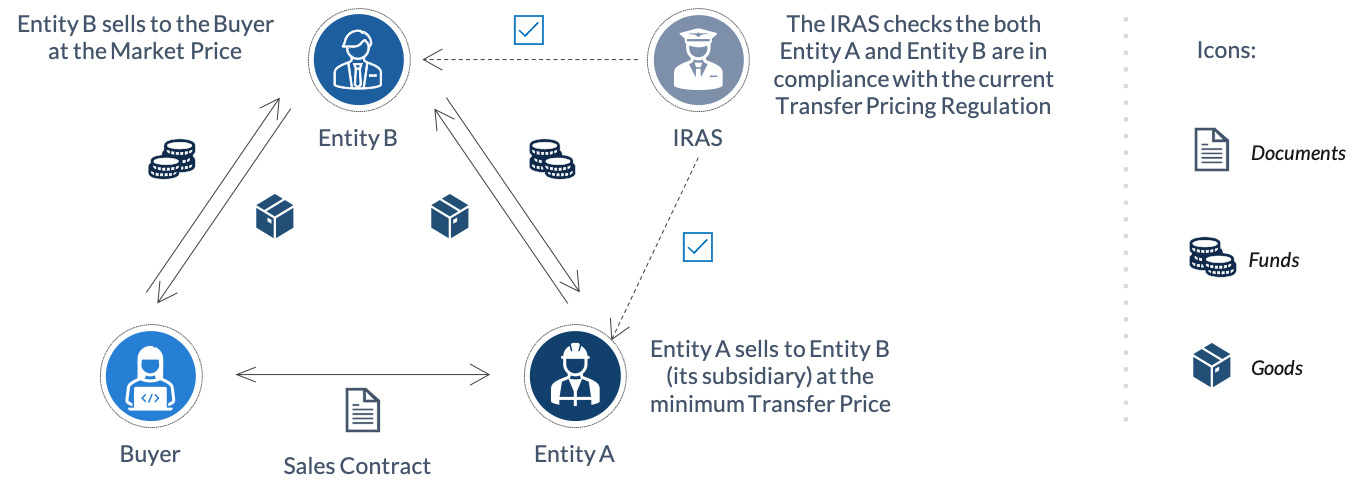

The “arm’s length principle”

The Inland Revenue Authority of Singapore (“IRAS”) applies the arm’s length principle, as legally prescribed in Section 34D of the ITA for purposes of pricing transactions between related entities. The arm’s length principle requires that terms and conditions negotiated between entities which are related by way of management, control or capital should be the same as that which would have been agreed between independent companies for similar transactions.

In Singapore, guidance on determining the arm’s length price is provided by the Singapore Transfer Pricing Guidelines, which falls outside the transfer pricing legislation.

Figure 1. The Arm’s Length Principle

Applying the arm’s length principle: a three-step approach

The IRAS recommends that Singapore entities follow a three-step procedure, which is neither mandatory nor prescriptive, for purposes of assisting businesses in ensuring that their transactions comply with transfer pricing regulations.

Step 1: Carry out a comparability analysis

Carrying out a comparability analysis ensures that a transaction between related entities has economically relevant characteristics which are similar to those of a transaction between non-related entities, as required by transfer pricing rules. Relevant aspects include the following:

a. Contractual terms of the transaction

In ascertaining the transaction between related parties, the contractual terms tend to be the starting point. This includes examining the written agreement between parties, as well as verbal arrangements and parties’ conduct.

b. Specific characteristics of goods, services or intangible assets

These characteristics are key in determining the value of the subject matter, and it is generally observed that products with better quality and more features tend to be sold for a higher price.

c. Functions performed, assets used, and risks assumed by parties

A functional analysis in this regard involves an assessment of the economically significant activities and responsibilities undertaken, assets used, and risks assumed by the transacting parties. These conditions between related parties in intragroup transactions should be equal to those between non-related parties.

d. Commercial and economic circumstances of parties

The commercial and economic circumstances in which the parties operate are relevant for purposes of this comparability analysis. It has been observed that prices for the same good or service may vary across different markets.

Step 2: Select the most suitable transfer pricing method

The IRAS uses several methods to evaluate a company’s transfer prices, based on prices adopted by non-related parties in similar transactions. The choice of method tends to depend on available data and relevant circumstances.

a. Comparable uncontrolled price method

This method compares the price in a related party transaction, with that in an independent party transaction in comparable circumstances. A difference between both prices may suggest that the parties are not dealing at arm’s length. The authorities may replace the price of the transaction accordingly.

It should be noted that relevant data may not be available for use of this method, especially where unique one-time transactions are concerned.

b. The resale price method

Where a product which was purchased from a related entity is resold to a non-related entity, both prices would be compared to ascertain if the price in the first transaction was fair, and whether the chain of transactions make economic sense.

c. Cost plus method

This method requires that the sale price of a product covers its manufacturing cost and generates additional profits.

d. Transactional profit split method

This method requires that related entities split the profits and losses of the transaction based on their relevant economic contributions.

e. Transactional Net Margin Method

This method involves a comparison of a company’s net profit margin in a non-arm’s length transaction with those realized in an arm’s length transaction. The net profit margin should also be examined relative to an appropriate base, such as costs, sales or assets.

Step 3: Determine the arm’s length results

To determine arm’s length results, the most suitable transfer pricing method will be applied in relation to the data of similar transaction(s) between non-related entities.

Implications

Where the pricing of a transaction between related entities is not at arm’s length and leads to lower profit and thus tax avoidance for a Singapore taxpayer, the IRAS may increase the profit of the Singapore company for tax purposes. To this end, Section 34D of the ITA provides that such adjustment may increase the amount of income or reduce the amount of deduction or loss the Singapore entity may claim.

Singapore’s transfer pricing documentation requirements

Under Singapore law, transfer pricing documentation is mandatory, pursuant to Section 34F of the ITA.

Transfer pricing documents must be prepared and kept by a Singapore company if its (a) gross revenue derived from its trade or business exceeds S$10 million for the tax basis period, or (b) transfer pricing documentation was explicitly requested by the IRAS for the basis period immediately before the basis period concerned.

The necessary documents, as provided in the Income Tax (Transfer Pricing Documentation) Rules 2018, include the following:

✓ An overview of the businesses of the entity’s group which are relevant to business operations in Singapore; and

✓ The entity’s business and transactions with related parties.

The transfer pricing documents must be completed by the filing due date of their tax return.

While Singapore companies are not required to submit these documents when filing a tax return, they are required to submit relevant documents within 30 days of a request for these documents by the IRAS.

These documents should be retained for at least 5 years from the end of the basis period in which the transaction took place.

A full list of documentation exemptions is prescribed in Section 4 of the Income Tax (Transfer Pricing Documentation) Rules 2018. These include related-party domestic transactions subject to the same tax rate, and related-party transactions with value not exceeding certain thresholds.

![]()

Figure 2. Mahanakorn Partners Group Transfer Pricing Services

Penalties

A Singapore company which fails to comply with transfer pricing documentation requirements may be liable to a penalty of up to S$10,000 for each offence, pursuant to Section 34F of the ITA. Moreover, Section 34D of the ITA provides that the company may be required to adjust the transfer price used in the relevant transaction based on a price determined by the authorities, with taxes to be paid based on the new price. It is noted that the taxpayer is subject to a surcharge of 5% of the amount of adjustment under Section 34E of the ITA.

Concluding remarks

In light of the right of the IRAS to adjust the pricing for related-party transactions that are not at arm’s length, as well as the mandatory transfer pricing documentation requirements, it is strongly advised that any internationalized group of companies with a Singapore entity should stay up to date with Singapore’s transfer pricing rules which govern the price of goods, services or intangible assets transferred between related entities within a group. Ultimately, these rules seek to prevent hidden profits, as well as preferential pricing which leads to underpayment of taxes.

For inquiries about tax liabilities, or any other aspect of cross-border trade and transfer pricing, please contact us at [email protected]