The Director-General’s Notification on Stamp Duty Tax (No.63) was recently gazetted on 5 October 2021. The Notification identifies additional instruments which have their contents prepared in electronic format and fall under the law governing Stamp Duty Tax for e-Instruments. This Notification is effective for e-Instruments executed from 6 October 2021 onwards.

Previously, the Notification of the Director-General of Revenue Department (No. 58) returned the payment of Stamp Duty for the following electronic instruments:

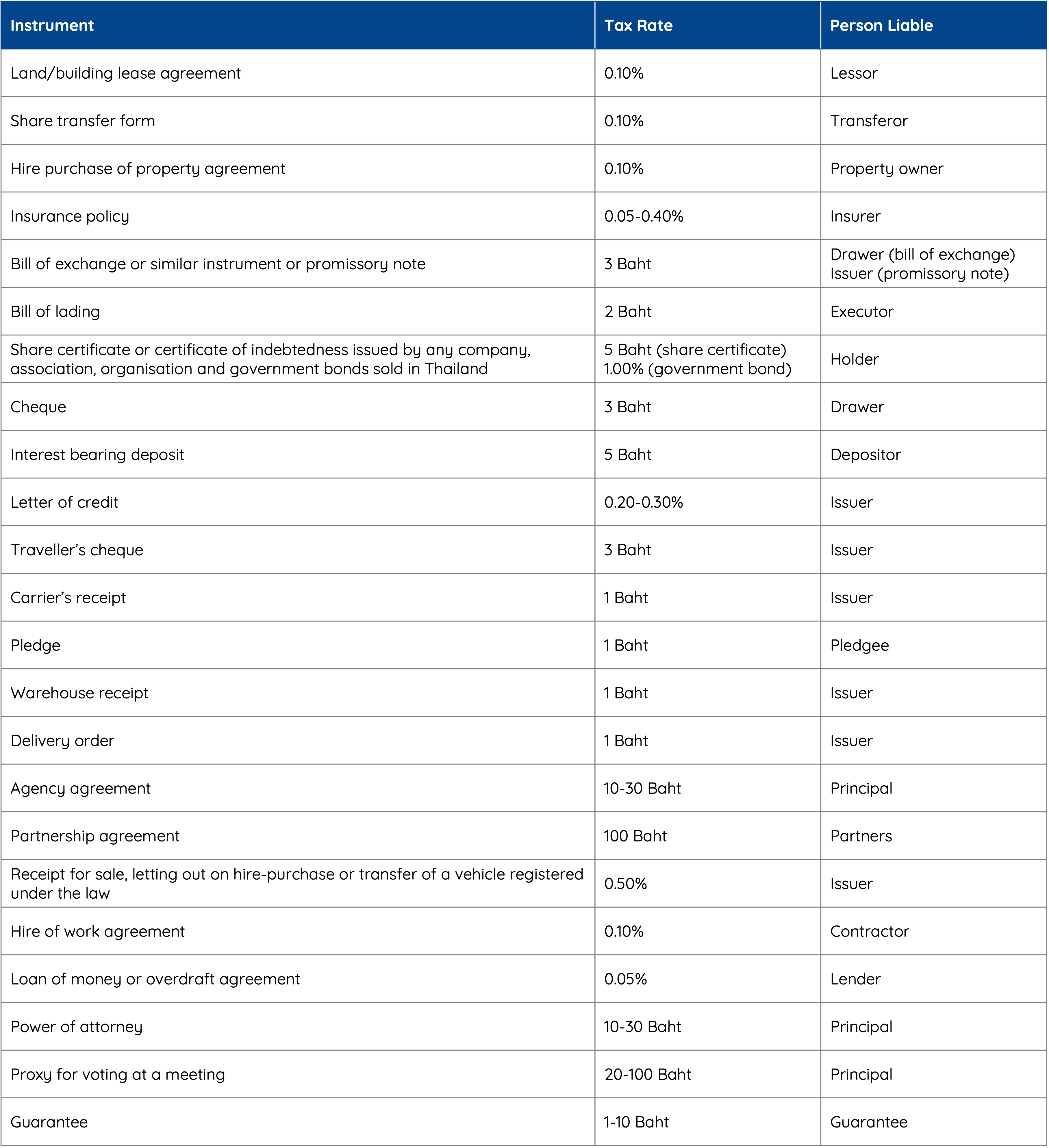

✓ Hire of work agreement

✓ Loan of money or overdraft agreement

✓ Power of attorney

✓ Proxy for voting at a meeting of a company

✓ Guarantee

The most recent Notification, (No. 63) amends the previous Notification (No. 58) to include the following 18 electronic instruments:

1. Land/building lease agreement

2. Share transfer form

3. Hire purchase of property agreement

4. Insurance policy

5. Bill of exchange or similar instrument or promissory note

6. Bill of lading

7. Share certificate or certificate of indebtedness issued by any company, association, organisation and government bonds sold in Thailand

8. Cheque

9. Interest bearing deposit

10. Letter of credit

11. Traveller’s cheque

12. Carrier’s receipt

13. Pledge

14. Warehouse receipt

15. Delivery order

16. Agency agreement

17. Partnership agreement

18. Receipt for sale, letting out on hire-purchase or transfer of a vehicle registered under the law

Method of Payment

The method of payment of the Stamp Duty Tax is changing as of 01 January 2022. From this date onwards, payment will only be allowed via the Revenue Department’s eFiling system. From 1 July 2019 to 31 December 2021, payment may be made either via the eFiling system or through payment in cash at a local Revenue Area office.

Deadline for Payment

The Stamp Duty Tax must be paid either before the execution of the e-Instrument or within 15 days of the date of execution of the e-Instrument.

A taxpayer who applies to pay an additional duty, or to make a late payment, must pay the applicable Stamp Duty Tax required as well as a surcharge and fine at the time of submission of the application.

Stamp Duty Tax Rates

The following tax rates apply to the electronic instruments that attract Stamp Duty: