Thailand Tax Ministerial Regulation No. 373 was gazetted on 11 June 2021, to grant and extend a reduction of the withholding tax rate for domestic payments from 1 October 2020 – 31 December 2022. The tax reductions are contingent on the entity or individual using the e-Withholding tax system. If the e-Withholding tax system is not used, the usual rate of withholding tax will be applied.

Under the domestic withholding tax system in Thailand, corporate entities are required to deduct withholding tax for payments to payees in Thailand. Within seven days of deduction, corporate entities must forward the withholding tax to the Thailand Revenue Department.

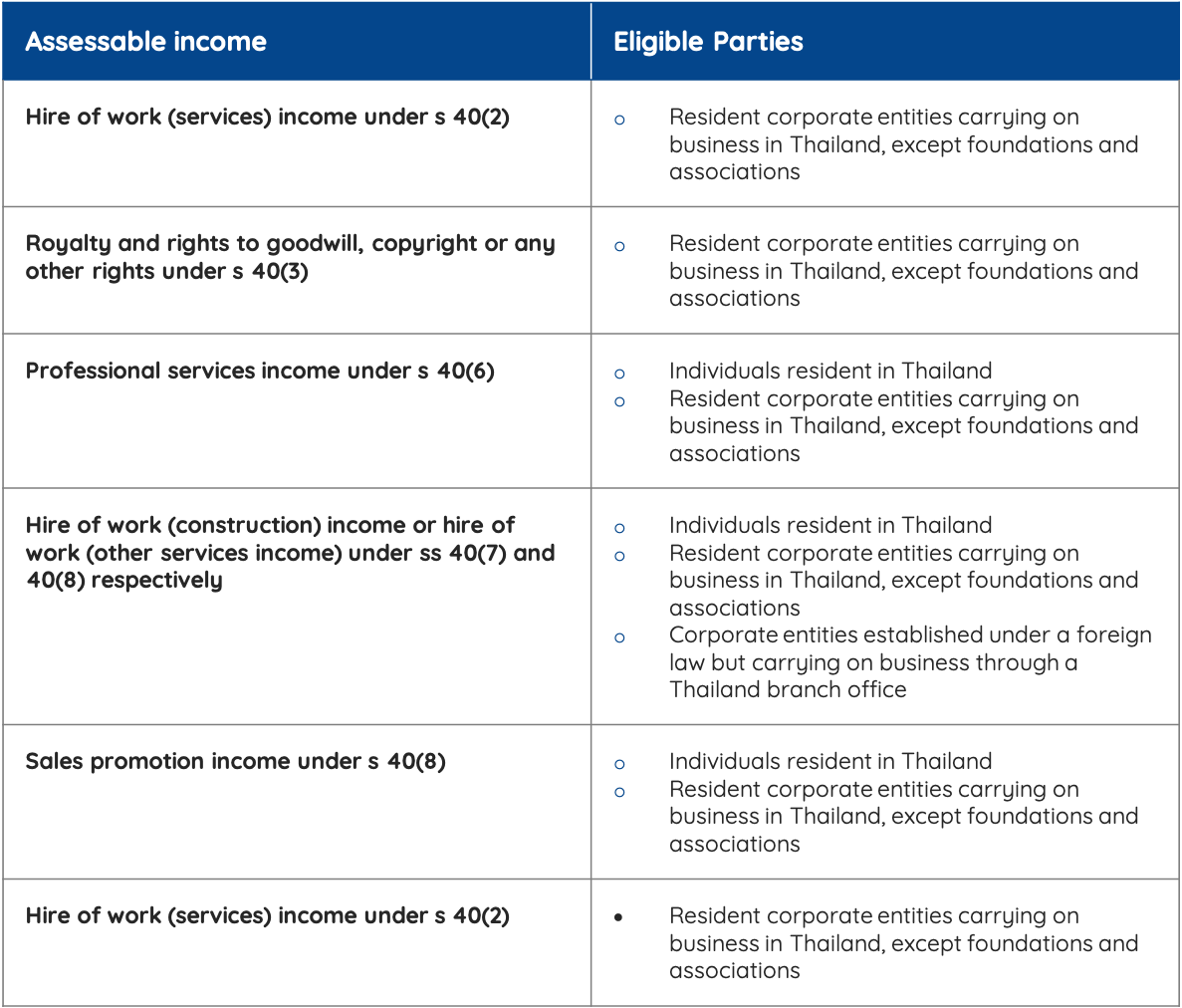

The Thai Revenue Code sets out the withholding tax rates required to be deducted. Based on the Revenue Code, the new reduction of the withholding tax rate from 5% to 2% is applicable to the following payments of assessable income:

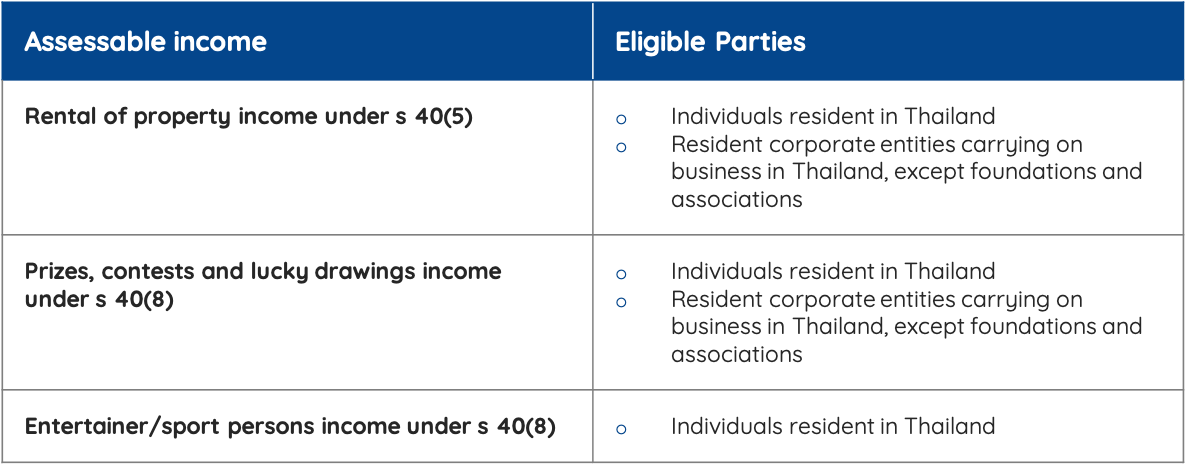

An extension of the withholding tax rate from 3% to 2%, originally due to expire on the 31 December 2021 has been continued until 31 December 2022 for the following assessable incomes: