As part of an initiative to assist debtors and borrowers struggling to service their debts, on 10 April 2021 The Emergency Decree amending the Civil and Commercial Code B.E 2564 (2021) was announced to reflect Thailand’s current economic climate and the capabilities of its debtors and creditors. The provisions focus on lowering the standard interest rate, default rate, as well as interest charging and calculations.

These amendments are effective as of 11 April 2021, any default or interest arising after this date, notwithstanding if the agreement was entered into before the Emergency Decree was enacted, are subject to the amendments.

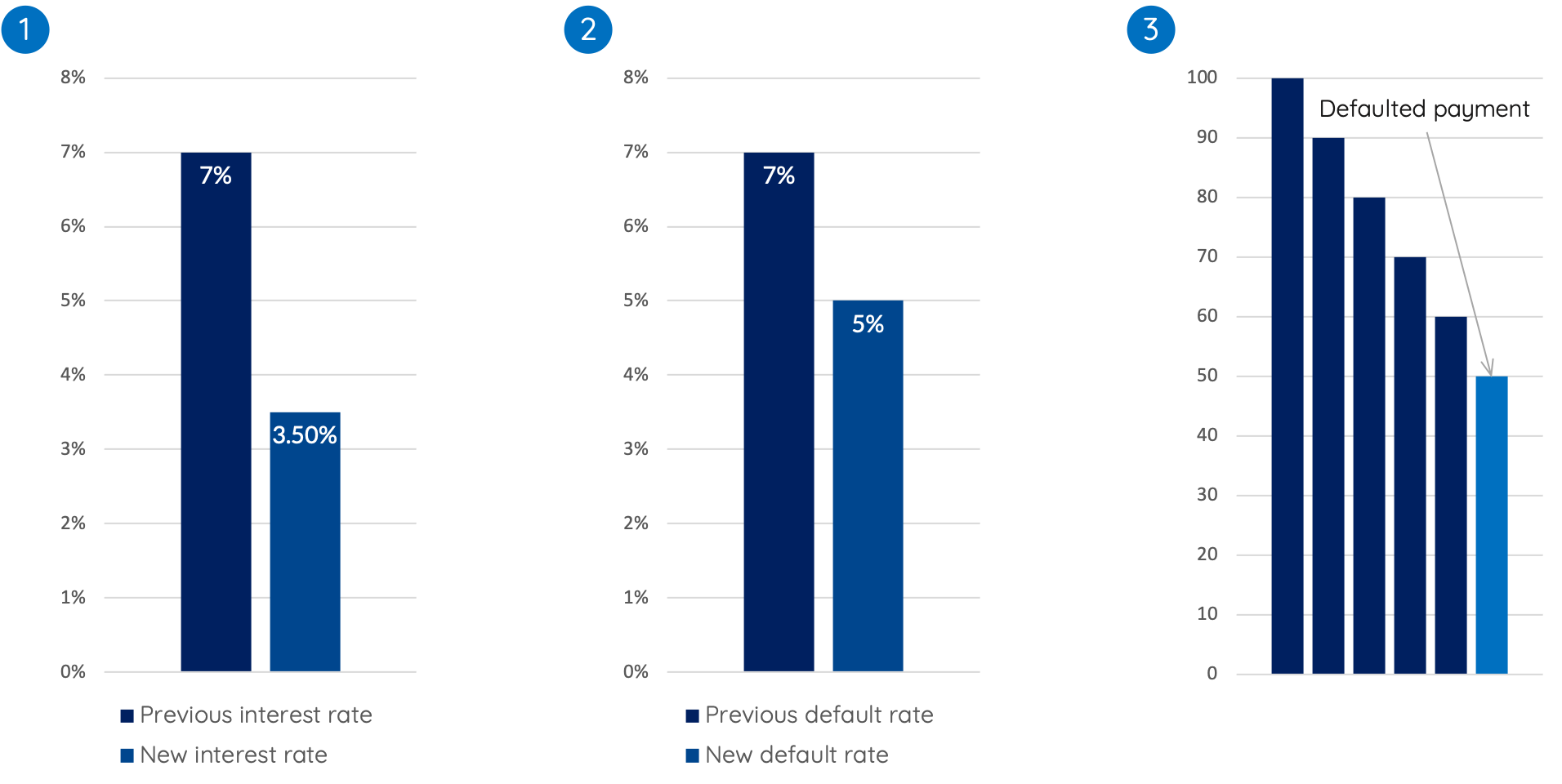

Three key changes brought in by the amendments

1. The first change revises the statutory interest rate under s 7 from the previous 7.5% per annum to 3% per annum. This rate is applicable in all circumstances where interest is payable, with the exception of the rate being fixed in an agreement or by an express provision of law. The statutory interest rate is subject to review by the Ministry of Finance every three years and can be amended by royal decree.

2. The second change concerns default rates under s 224 of the CCC. Previously, where there was a default on a payment, a creditor would automatically charge a default rate of 7.5% (or higher if there were established legal grounds to do so). The new statutory default interest rate sits at 5% per annum. This amount is calculated from the amended 3% per annum statutory interest rate under s 7, with an added-on rate of 2%. The default rate is in part based on the statutory interest rate and will therefore change along with s 7.

3. Finally, the newly enacted s 224/1 provides that where a debtor fails to make an instalment payment, a creditor is entitled to the default interest based only on the amount of the default instalment. This precludes creditors from being able to claim a default interest on the whole amount of an unperformed obligation. Any agreement seeking to exclude or vary this provision is null and void.

Implications

While the s 7 and s 224 amendments are undoubtedly a positive initiative to reduce the high interest rates previously imposed on debtors, it is unlikely that the amendments will have a major effect. The statutorily imposed standard interest rate and default interest rate are not applicable where an agreement or provision of law provides otherwise. This has effectively given parties the ability to “contract out” of the statutory rate and impose higher standard and default interest rates. Therefore, it is likely that these amendments will only have an impact on small financing transactions.