On the 29th day of December 2022, the Revenue Department issued a Notice relating to Income Tax (No. 431) on income paid for buying goods or services. The Notice took effect from the 1st of January 2023.

The principles, procedures and conditions regarding such income are prescribed below, pursuant to Article 1 and Article 2 of the Ministerial Regulations No. 186 (B.E. 2565 (2022)) issued under Revenue Code Governing Exemption of Taxes and Duties.

Evidence of Payment

In exercising the right of income tax exemption on income paid for buying goods or services for up to 40,000 baht, an income earner must provide tax invoices (under Section 86/4 of the Revenue Code) or receipts as evidence. This evidence must contain at least the particulars under Section 105 bis of the Revenue Code and must specify the income earner’s full name according to the following principles, procedures and conditions:

Following Section 3 sedecies of the Revenue Code:

✓ Tax invoices or receipts as evidence for amounts up to 30,000 baht may be in electronic or paper format to exercise the right of income tax exemption.

✓ Tax invoices or receipts as evidence for amounts between 30,000 baht and 40,000 baht must be electronic only to exercise the right of income tax exemption.

The electronic tax invoices or the receipts under paragraph one must be prepared by the value added tax (VAT) registered operators or the persons liable to issue receipt as per the list published under Article 12 of the Ministerial Regulations No. 384 (B.E. 2565 (2022) Issued under Revenue Code Governing Proceedings Relating to Documentary Evidences or Letters by Electronic Means.

This is effective between the 1st of January 2023 and the 15th of February 2023.

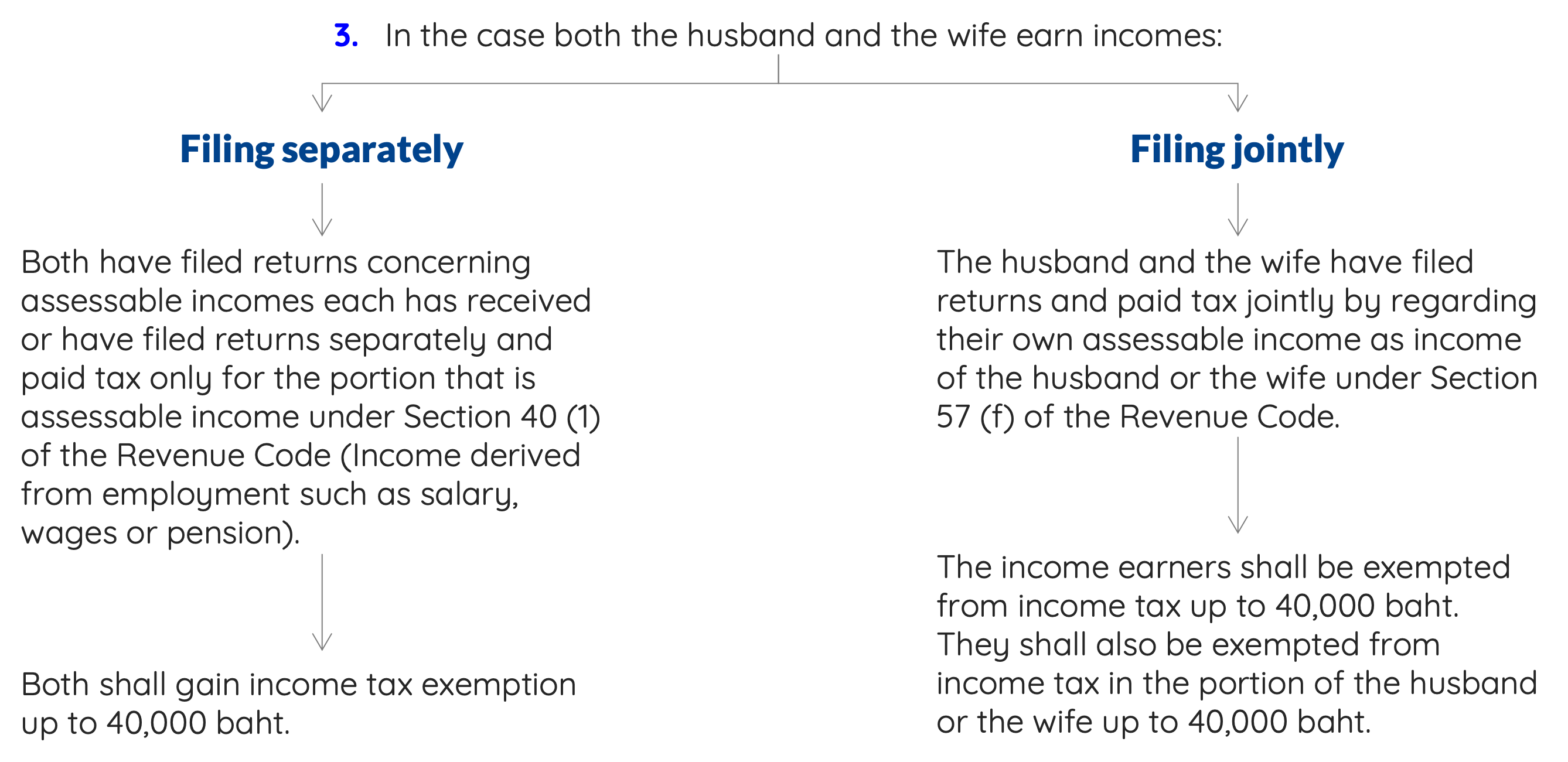

Spousal Application of Income Tax Exemption

The exemption of income tax for a person liable to pay natural person income tax must be according to the following principles:

1. The income earner shall be exempted for up to 40,000 baht given they are not an ordinary partnership or organization that is not a juristic person.

2. If only the husband or wife earns income, income tax shall be exempted for the spouse who earns income according to the amount paid up to 40,000 baht.

Formal Requirements

Goods and services must be bought in Thailand and the receipts of purchase must contain different particulars if the vendor is VAT registered or not, or if the product is in the “One Tambon One Product Program”.

Exercising income tax exemption under this Notice requires an income earner to buy goods or services within Thailand between the 1st of January 2023 and the 15th of February 2023.

The purchases must also be according to the following conditions:

|

When paying for books or book service fees in electronic data format via internet systems: |

If the vendors are a VAT registered operator, tax invoices must be received under Section 86/4 of the Revenue Code. |

|

If the vendors are not a VAT registered operator, there must be receipts containing at least the particulars under Section 105 bis of the Revenue Code and the income earner’s full name. |

|

|

When buying goods in the One Tambon One Product Program: |

If the vendors are a VAT registered operator, the said goods must be registered with the Community Development Department, and tax invoices must be received from the vendors (under Section 86/4 of the Revenue Code). |

|

If the vendors are not a VAT registered operator, receipts must be received containing at least the particulars under Section 105 bis of the Revenue Code mentioned above. They must also have the income earner’s full name. |

The Revenue Code states the following particulars under Section 105 bis:

✓ Taxpayer identification number of the receipt issuer;

✓ Name or label of the receipt issuer;

✓ Serial numbers of the book and of the receipt;

✓ Date of issuance of the receipt;

✓ Amount of payment received;

✓ Type, description, quantity, and price of the goods, only in the case of sale or hire- purchase of certain types of goods with a price of 100 baht or more.

In preparing the name, type, and category of goods in the tax invoice under Section 86/4 (5) of the Revenue Code or in the receipt, the sellers must do the following:

✓ Specify a statement showing that the said goods are products from the One Tambon One Product Program for each item of goods or make a symbol showing that each item is a product from the One Tambon One Product Program and have a statement showing that the said symbol refers to the products from One Tambon One Product Program on the tax invoice or the receipt, such as “OTOP”, “โอทอป”, or “One Tambon One Product”.

✓ If all goods in the tax invoices or receipts are products from One Tambon One Product, and a statement or a symbol under (1) is not specified, the vendors who issue the tax invoices or receipts must affix a rubber stamp bearing their trade name or trademark with statement on the tax invoice or the receipt reading “All Items of Goods Are Products from One Tambon One Product Program” (“สินค้าทุกรายการเป็นสินค้าหนึ่งตำบล”), or similar.

When buying goods or services other than those mentioned above, it must be made to the VAT registered sellers of goods or the service providers and who must receive tax invoices under Section 86/1 of the Revenue Code. The income paid for buying goods or services which are entitled to income tax exemption must be for the buying goods or receiving of services that must specifically be included for calculation as a tax base at the rate of 7%.

The impact of VAT calculation on income tax exemption under this notice

If the VAT registered operator, as an income earner, has deducted the value added tax in the tax invoice from the sale tax in calculating the VAT under Section 82/3 of the Revenue Code, they cannot use the payment for buying goods or services under said tax invoice for income tax exemption.

For income tax exemption under this Notice, the income earner may deduct it from the assessable income under Section 40 of the Revenue Code after deduction of expenses under Section 42 bis to Section 46 of the Revenue Code.