Thailand continues efforts to promote scientific and social development in a recent Royal Decree (“RD”) granting income tax exemptions for investment in target companies. The RD Issued under Revenue Code Governing Exemption of Taxes and Duties (No. 750) B.E. 2565 (2022) became effective June 15th, 2022, and remains in effect until June 30th, 2032.

This RD is primarily designed to exempt gains, earn by natural persons, companies, and juristic partnerships, that have invested in companies or juristic partnerships engaged in target industries (“Target Companies”). The exemption also applies to investments made in qualifying Thai private equity companies (“PE”), and Thai venture capital trusts (“VCT”), which themselves have invested in Target Companies.

To qualify as a Target Company, the operating company or juristic partnership must operate a business that engages in one or more of the following “Target Industries”. Target Industries have been identified by The Committee on Policy for National Competitiveness Enhancement for Target Industries:

✓ Next generation automotive

✓ Intelligent electronics

✓ Advanced agriculture and biotechnology

✓ Food for the future

✓ High-value and medical tourism

✓ Automation robotics

✓ Aviation and logistics

✓ Medical and comprehensive healthcare

✓ Biofuels and biochemicals

✓ Digital development

✓ Defense

✓ Education and human resource development

Additional specifics are as follows:

1. Direct Investments. Gains arising from the transfer of shares in a Target Company will be exempt from personal income tax (“PIT”) or corporate income tax (“CIT”). Important conditions include:

a. The investor must have held the shares for at least twenty-four (24) months before the capital gain incurs; and

b. At least 80% of the Target Company’s operating revenue must have arisen from business operations in Target Industries in each of the two (2) consecutive accounting periods prior to earning gains from the transfer of shares.

2. Investments Through PEs

a. Share Transfer Gains. Gains arising from the transfer (disposal) of shares in a PE, which, invests in a Target Company, will be exempt from PIT and CIT provided that the investor held those shares of the PE for at least twenty-four (24) months before the capital gain incurs. Furthermore:

i. If the PE has no retained earnings, the capital gain exemption is only in proportion to the PE’s investment in Target Companies. Additionally, at least 80% of the Target Company’s operating revenue must have arisen from business operations in Target Industries in each of the two (2) consecutive accounting periods prior to the day gains are earned from the transfer of shares. The required proportion of investments into Target Companies by the PE shall be prescribed by the Director General (“DG”) of the Revenue Department.

ii. If the PE does have retained earnings, and at least 80% of retained earnings arose from gains as described in I above, in each of the two (2) accounting periods prior to the date which the investor into the PE earns revenue from the transfer of shares (of the PE), then the entire gain earned by the investor into the PE will be exempt from PIT or CIT.

iii. Legal reserves may not be counted as part of retained earnings in i. and ii. above.

b. Dissolution Gains. Generally, upon dissolution, if a shareholder receives a return on investment exceeding the cost of investment, that excess is considered income for tax purposes (RC, Section 40 (f)). However, under this RD, such excess return of capital from the dissolution of a PE is exempt from income recognition for the PE investor. The exemption is limited in that it is available only in proportion to the PE’s investment in Target Companies. Furthermore, at least 80% of the Target Company’s operating revenue must have arisen from business operations in Target Industries in the two consecutive accounting periods before the dissolution of the PE.

3. Investments Through VCTs

a. Unit Transfer Gains. Gains arising from the transfer (disposal) of units in a VCT, which were invested in a Target Company, will be exempt from PIT and CIT provided that the investor held the shares for at least twenty-four (24) months before the gain arose. Furthermore:

i. If the VCT had no retained earnings, the capital gain exemption is only in proportion to the VCT’s investment in Target Companies. Furthermore, at least 80% of the Target Company’s operating revenue must have arisen from business operations in Target Industries in each of the two (2) consecutive accounting periods before the gain from the transfer of units arises. The required proportion of investment in Target Companies by the VCT shall be prescribed by the Director General (“DG”) of the Revenue Department.

ii. If the VCT has retained earnings, and it had retained earnings, in each of the two (2) accounting periods proceeding the unit transfer, which arose from investment in a Target Company, which has earned at least 80% of its total income from business in target industries, then the entire gain from transfer of units will be exempt from PIT or CIT.

b. Dissolution Gains. The revenue earned by a unit holder in a VCT, upon dissolution of that VCT is exempt from income recognition, however only in proportion to the VCT’s investment in Target Companies. Furthermore, at least 80% of the Target Company’s operating revenue must have arisen from business operations in Target Industries in each of the two (2) consecutive accounting periods proceeding the VCT’s dissolution.

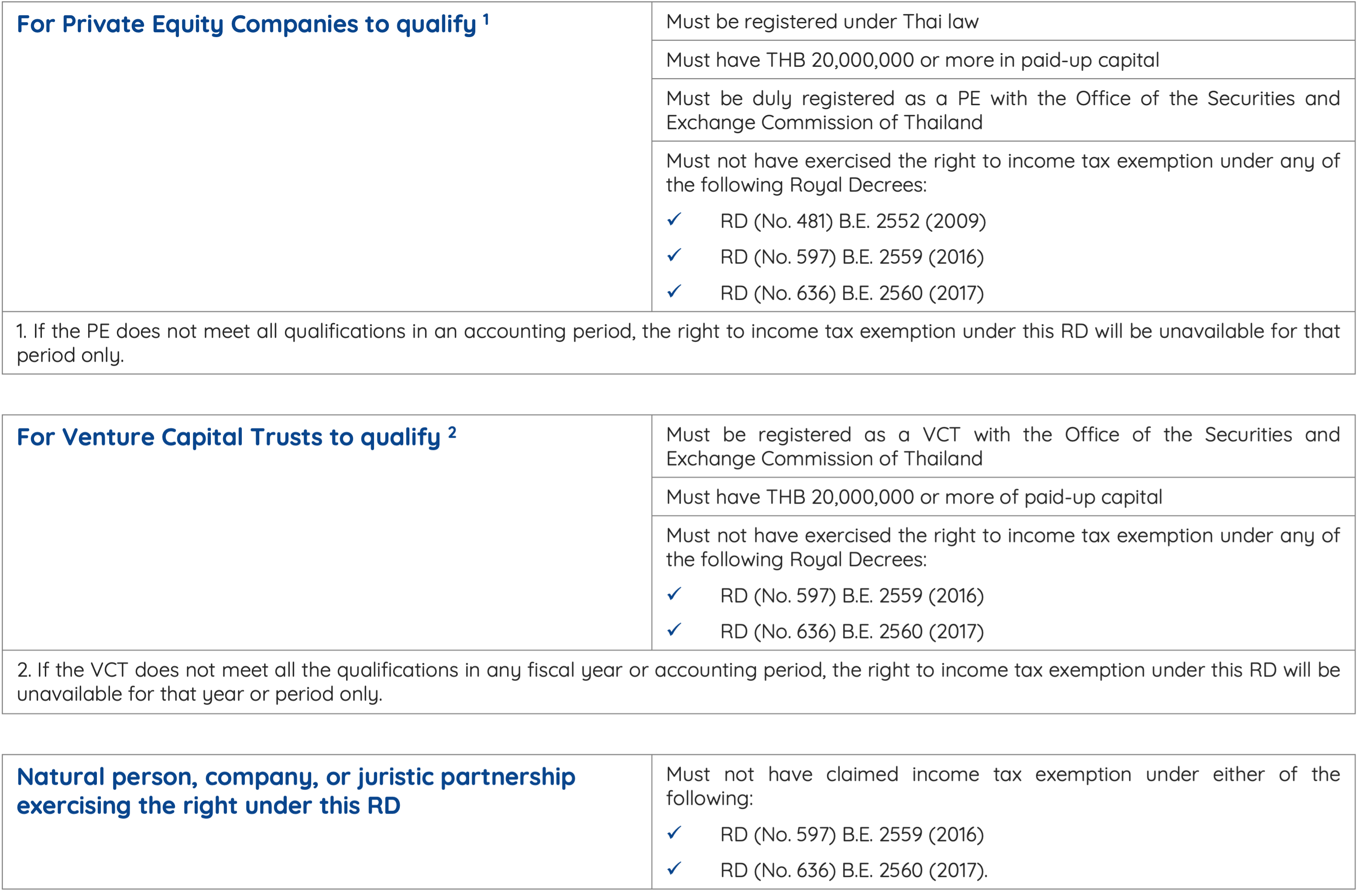

Additional conditions apply to benefit from the tax exemption under this RD and include the following: