Logistics System Efficiency

Situated at the heart of the Mekong Region, Thailand is a Kingdom with 76 provinces. Its geographic position grants it access to the world’s largest consumer markets, namely China, India and ASEAN. Consequently, Thailand is rapidly enhancing its infrastructure and logistics development, and is poised to become ASEAN’s transportation and logistics hub. Thailand’s USD 25.2 billion national infrastructure development program includes several rail and road greenfield and brownfield projects, public transport enhancement, airport expansion, and seaport development nationwide. Major plans include:

✓ U-Tapao airport development

✓ Sattahip, Laem Chabang, and Map Ta Phut seaport upgrades

✓ High-speed and double-track railways

✓ Bangkok’s public transport network expansion

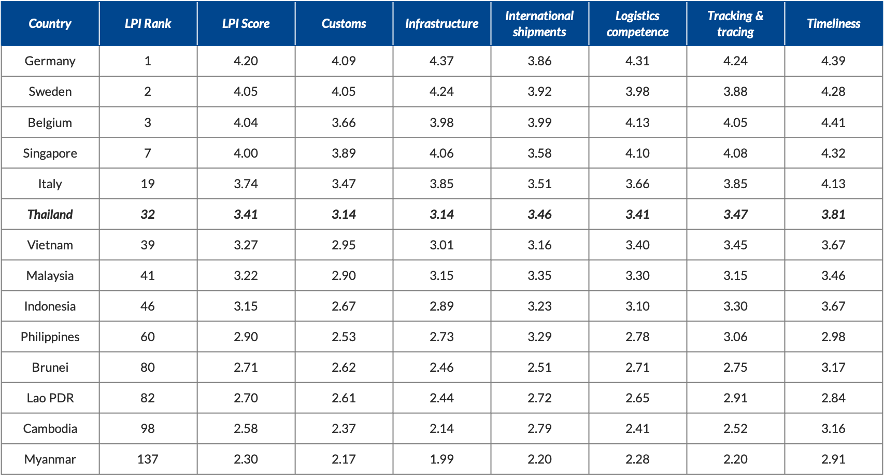

In 2017, the logistics market in Thailand was a USD 63.1 billion market and estimates predict it soar to USD 83.7 billion by 2022. Freight transport by road dominates the Thai logistics sector. Thailand ranks 32nd in the World Bank’s Global Logistics Performance Index and is second only to Singapore in ASEAN. Thailand’s infrastructure quality and overall logistics performance is expected to continue to improve in the future, as a result of the many infrastructure projects in the 2017 Transport Infrastructure Action Plan pipeline.

As a consequence of the COVID-19 pandemic, the Kingdom’s consumer market—the ASEAN region’s largest online population and second largest economy—has increasingly shifted to e-commerce. Meanwhile, Thailand’s maritime, air and road transportation services are all tipped for stronger rebound consistent with the pickup in world demand.

The Trade Policy and Strategy Office (TPSO) database shows that, as of August 2020, over twenty thousand Thai companies were registered in the logistics sector. Most of these are active in road and rail transportation, many in warehouses and related activities, and a few hundreds in maritime shipping, air transportation and delivery services.

Thriving Delivery and Goods Transportation

According to a study conducted by JP Morgan, thanks to the sophisticated and coordinated Thai transportation systems, about ⅓ of all e-commerce activities in Thailand can be categorized as cross-border transactions, while ½ of online Thai shoppers have purchased goods from abroad. The top three overseas destinations for Thai exports are China, Japan, and the United States.

In recent years, Thailand has set aside at least USD 25 billion for rail/road upgrades, public transportation development, and air/sea development. This should significantly bolster the general system for years to come. Thai air freight is expected to prosper between 2021 and 2023, and Thai shipping volume should increase to as much as 536 million tons by 2039.

Road transportation is expected to become more important than in the past and facilitate cross-border transactions. We may see industrialization not only in and around Bangkok but further afield in Thailand and ASEAN states, which will bolster Thai transportation systems.

Promising Hub for Maritime, Air, and Road Logistics

Thailand’s logistics industry has declined because of Covid-19 but is already showing signs of a gradual recovery, along with world demand for Thai exports and tourism. The Kingdom’s long-term and ongoing investment in upgrading its deep seaports and international airports aims at underpinning the growth of the logistics industry and cement Thailand as an Asia-Pacific logistics hub.

Inasmuch as about 90% of imports and exports rely on maritime transport, expanding the capacity of its seaports was a priority for the Kingdom. Flagship projects include the expansion of two deep-sea ports in the EEC, namely Laem Chabang Deep Seaport poised to reach a capacity of at least 18 million TEUs per year upon completion (targeted in 2023), and Map Ta Phut Industrial Seaport to increase the capacity of natural gas and fluid material shipments for the petrochemical industry upon completion (targeted in 2025).

The Thai aviation industry and air freight business has grown constantly since it underwent liberalization in 2008. Air freight is expected to grow back to the pre-Covid level of 61.2 million tons in 2021, compared with 54.2 million tons in 2020. Thailand’s ongoing investment in upgrading the capacity of Suvarnabhumi, Don Mueang, and U-Tapao international airports, major provincial airports, as well as the Eastern Aviation City, which includes maintenance repair and operation (MRO) facilities, is expected to support Thailand’s position as a regional logistics hub.

Road transportation accounts for 80% of all goods carried for industrial, farm, construction materials, and delivery sectors. Thailand relies on a masterplan of public-private partnership (PPP) projects plans to upgrade its infrastructure, focusing on dual-tracked railways connecting with motorways, airports, and seaports. Under the Motorway-Rail Map, the Thai government plans to invest in the construction of dual-tracked railways linking Bangkok to major provinces and regional economic corridors (e.g., the China-Laos Railway).

Smart Warehouses as the Heart of the Supply Chain

Boasting the largest e-commerce market in ASEAN, Thailand’s warehouses have grown rapidly, and attract more investors to the EEC and other Special Economic Development Zones. Despite the slowdown in the global economy during the pandemic, the total warehouse supply in Thailand increased by 2.5%, with occupancy standing at approximately 85% at the end of 2020.

To tackle the challenges in supply chain management, many warehouses in Thailand have installed upgraded systems, such as enterprise resource planning, cloud-based warehouse management systems, and automation and robotics, to enhance their competitiveness and support the Kingdom’s vibrant trade and logistics ecosystem.

World Bank’s Global Logistics Performance Index (2018)

The Logistics Performance Index (LPI) is an interactive metric benchmarking 160 countries. The LPI is based on a global survey of field operators, who provide feedback on the logistics friendliness of target countries. Operator feedback is supplemented by quantitative data on the performance of key components of the supply chain in the country in which they operate. Thus, the LPI consists of both qualitative and quantitative measures and helps build logistics friendliness profiles for these countries. It measures performance along the supply chain within a country and offers two distinct perspectives: international and domestic.

Table 1. Logistics Performance Index (from 1 = Low to 5 = High).