In recent years, Thailand has emerged as a pivotal player in the mergers and acquisitions (M&A) landscape of Southeast Asia. This comprehensive analysis delves into the transformative journey of Thailand’s M&A activities from 2019 to 2024, highlighting key trends, landmark deals, and the resilience of Thai companies amidst global uncertainties. From a pre-COVID surge driven by favorable economic conditions to a pandemic-induced slowdown and subsequent robust recovery, the Thai M&A market has navigated through significant challenges and opportunities. This period has not only underscored the strategic agility of Thai enterprises but also positioned Thailand as a formidable force in the global M&A arena.

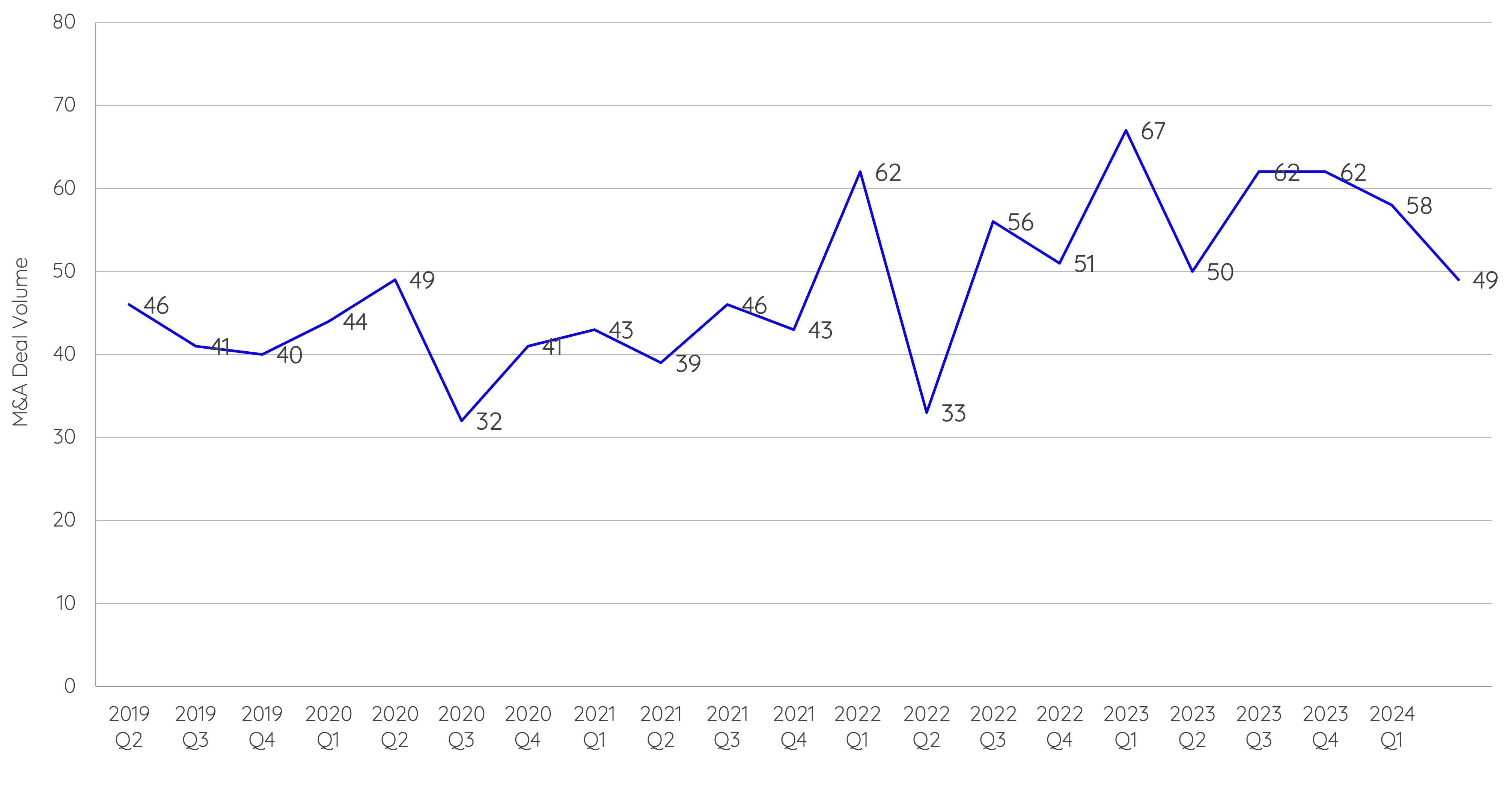

Figure 1. M&A Deal Volume 2019-2024.

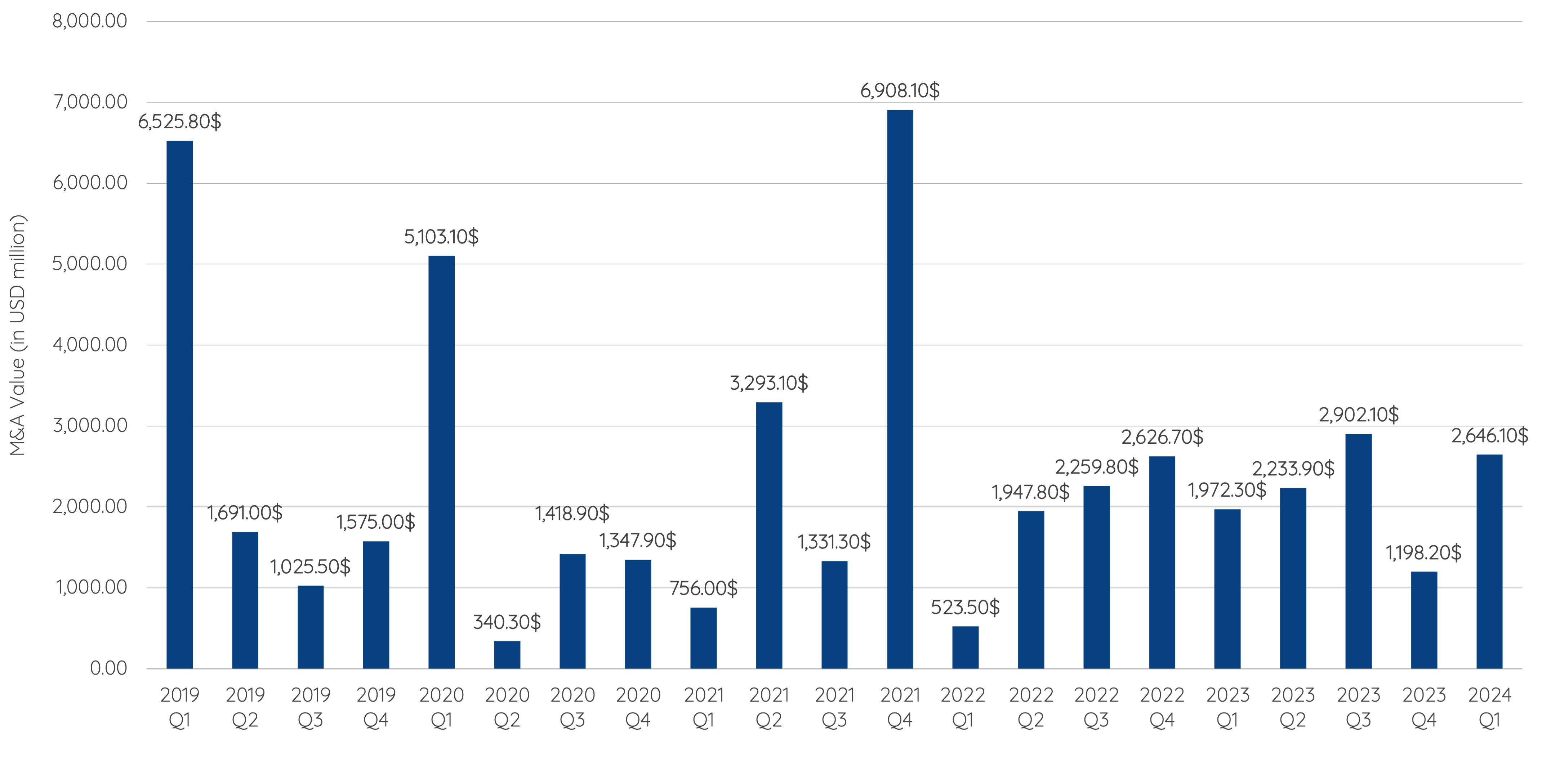

Figure 2. M&A Deal Value (in USD million) 2019-2024.

Pre-Covid: A Surge in Cross-Border Activity

The year 2019 was a remarkable one for Southeast Asia, with cross-border acquisitions reaching unprecedented heights. Thailand, in particular, stood out, contributing a significant 67% to Southeast Asia’s total deal value. The region saw 67 cross-border acquisitions amounting to $9.6 billion, nearly three times the value recorded in 2018. This surge can be attributed to a weakened baht and low interest rates, which made Thai companies more inclined towards overseas acquisitions as a strategy to mitigate domestic economic challenges.

A landmark event in this period was CP Group’s acquisition of Tesco’s Asian operations in March 2020. This deal, valued at approximately $10.6 billion, underscored Thailand’s growing prominence on the global M&A stage. Such substantial outbound investments were indicative of the strategic shift among Thai companies, seeking growth and diversification in international markets.

During Covid: A Period of Uncertainty and Slow Recovery

The onset of the COVID-19 pandemic in early 2020 brought a sharp decline in global M&A activity, and Thailand was no exception. The uncertainty caused by the pandemic led to a significant slowdown in the second quarter of 2020. However, the latter half of the year showed signs of cautious optimism. With historically low interest rates, companies with strong balance sheets began to eye distressed assets, setting the stage for a tentative recovery.

In 2021, the Thai M&A landscape started to recover as businesses adapted to the new normal. The easing of lockdown measures and a more stable economic environment facilitated this rebound. A notable transaction during this period was Central Group’s acquisition of Selfridges, highlighting the resurgence in deal-making activities. By 2022, as COVID-19 restrictions eased further, sectors like manufacturing, retail, and hospitality saw renewed M&A interest. The proposed merger between True Corporation and dtac signified significant movements within Thailand’s telecom sector, reflecting broader market adjustments to evolving consumer behaviors.

Post Covid: Resilience and Growth

The year 2023 marked a period of robust recovery and growth for Thailand’s economy, driven by a projected 3.6% GDP expansion. The resurgence of the tourism sector, along with government stimulus measures and a weakening baht, contributed to this positive outlook. M&A activity mirrored these economic improvements, with the first half of the year witnessing 62 deals totaling $2.3 billion.

One of the standout transactions was Avaada Energy Private Limited’s successful fundraising of $1.3 billion for solar power projects in India, supported by GPSC and Brookfield Renewable. This highlighted the increasing interest in sustainable energy investments. The latter half of 2023 saw continued momentum, with deal value growth of 30% to over $2.9 billion. Key sectors driving this growth included Industrials, Real Estate, Infrastructure, and Construction, which collectively accounted for 56% of the total deal value. Banpu Power PCL’s strategic acquisition of a gas-fired power plant in Texas exemplified Thai companies’ ambitions to expand their global footprint.

Despite a slight decline in deal value towards the end of 2023, the overall trend remained positive. The final quarter of the year saw Thai companies dominating the M&A scene, accounting for 80% of the total deal value. This period underscored a strategic focus on domestic investments while maintaining a steady stream of outbound deals.

Q1 2024: A Strong Start

The first quarter of 2024 witnessed a significant uptick in M&A activity in Thailand, with transaction values doubling compared to the previous quarter. While there was a slight reduction in the number of deals, key sectors such as Financial Services, Healthcare & Life Sciences, and Consumer & Retail continued to demonstrate strong performance. Noteworthy transactions included SCB’s acquisition of Home Credit Vietnam Finance Co., Ltd., and PTT’s divestment of Alvogen Malta, highlighting the resilience and strategic agility of Thai companies.

![]()

Figure 3. Transaction Value by industry in percentage per quarter.

Conclusion: A Dynamic M&A Landscape

Over the past five years, Thailand’s M&A landscape has demonstrated remarkable resilience and adaptability. From the pre-COVID surge in cross-border acquisitions to the pandemic-induced slowdown and subsequent recovery, Thai companies have strategically navigated through global uncertainties. The continued growth in 2024 underscores the strength and dynamism of Thailand’s corporate sector, positioning the country as a significant player in the global M&A arena. As Thailand moves forward, it remains well-poised to capitalize on emerging opportunities, driven by robust economic fundamentals and a proactive approach to strategic investments.