As the business world continues to globalize, more than ever international and multinational enterprises are seeking to expand into other markets. In recent years, with increased labor costs and regulations, certain countries that used to be favored, such as China, are becoming less optimal. Now, Southeast Asia, specifically Thailand, is becoming a very attractive choice. Thailand has a modern market, affordable and skilled labor force, and is a perfect gateway to Asia Pacific.

When seeking expansion, American companies must tackle two major challenges. First of all, determine the strategy to enter the new market. There are many options, from forming a new foreign business to an acquisition of an existing business. Next, due to FATCA and increased scrutiny on U.S. international tax reporting, businesses have concerns about potential U.S. compliance questions.

Entering the Thai Market

When entering the Thai market, foreign investors have several options. Sometimes, when greenfield investments may present unnecessarily high risks and costs, M&A transactions offer an alternative, and oftentimes financially viable, foreign direct investment solution. The following is a high-level overview of the investment options.

Figure 1. Common Market Entry Strategies

What are Mergers and Acquisitions?

Generally, mergers and acquisitions (M&A) refers to the transactions in which a company combines or consolidates in some form with another entity. The definition of M&A is intentionally broad, as M&A can include obtaining a company’s assets as well as its equity. While the two terms ‘mergers’ and ‘acquisitions’ are often used interchangeably, they differ in legal meaning and in practice.

M&A is useful in that it can help an entity leverage competitive advantage through growth, downsizing or changing the nature of its business operations.

Mergers

A merger is the process by which two companies combine to form a new legal entity under the same corporate name. For example, Company A will purchase Company B and continue operations under the Company A name. In a merger transaction, the acquired company’s assets are bought by the purchasing company, meaning that after the transaction is concluded only the purchasing company survives. Generally, the size of the purchasing company is relatively larger than the purchased company. The purchasing company (also known as the absorbing company), will acquire all the assets and liabilities of the absorbed company.

In terms of shares and ownership, the shareholders of the absorbing company keep their ownership, whereas the shareholders of the absorbed company are given shares of the absorbing company.

A merger is a corporate strategy often used to increase the financial and operational strengths of both companies.

Amalgamations

An amalgamation is a type of merger process. However, it should be distinguished from a merger, as not all mergers are amalgamations. An amalgamation occurs when two companies combine to form a larger single company, with neither of the previous companies remaining in independent operation. Effectively, a new company is created and neither of the existing companies survive. For example, Company A and Company B combine to operate as Company C. Effectively, an amalgamation actually involves three companies, the two existing companies and the new entity that is created. The assets and liabilities of both existing companies are transferred into the balance sheet of the newly formed company. Amalgamation often occurs between similar sized companies that operate in the same industry, thus resulting in reduced operational costs. Amalgamation is useful in that it can be used to access new markets, technologies, and geographies, among other aspects.

Acquisitions

An acquisition refers to the purchase of a corporate asset or target company. After the acquisition, the buying company obtains more than 50% ownership in the target company. In a simple acquisition, the purchasing company merely obtains majority stake in the target company, which does not change its name or organisational structure. For example, Company A acquires Company B and they continue to operate as the existing entity of the two separate companies. The result being, that both companies survive and continue to operate.

Types of Mergers and Acquisitions

Conducting a merger or acquisition is a dynamic and complex process which poses many challenges for the businesses involved. The process may differ depending on the type of M&A transaction being undertaken. There are three main types of M&A transactions depending on the relationship between the merging companies.

Horizontal

Generally, a horizontal merger is one between two companies in the same industry sector. The companies are in direct competition and share the same markets. An example is when one book publishing company purchases another book publishing company. This can be beneficial in that it can help increase market share, expand market opportunities, and save costs .

Vertical

A vertical merger is between a customer and company or supplier and company. For example, an ice-cream making company merges with a company that supplies ice-cream cones. A vertical M&A can assist in reducing overhead cost of operations.

Conglomerate

A conglomerate M&A refers to the process where the two companies are more or less unrelated. The objective here is often diversification of goods and services.

Risks of Mergers and Acquisitions

M&A transaction usually offer growth opportunities; however, there are some substantial risks that entities must be aware of before becoming before engaging in an M&A deal.

Lack of Due Diligence

Proper due diligence is critical for preparing a successful M&A transaction. Prior to entering into the transaction, the buying or acquiring company should ensure to learn as much as possible about the target or acquired company. Essential information to be analysed includes the company’s financials, contracts, customers, insurance, any outstanding litigation and any other information that will ensure a holistic understanding of the company.

Weak due diligence can expose a company to increased risks, such as poor valuation, litigation and tax issues.

Overpayment

Overpaying for a company is a common error committed by purchasing companies and can have extremely detrimental implications including destroying shareholder value. There is often considerable tension surrounding an M&A transaction and there may be pressure not only from the seller, but also internally and from intermediaries involved in the transaction. Overpayment is one of the major and regular mistakes in M&A agreements, with the root of the problem often coming down to a highly pressurized environment and poor valuation practices.

The overall strategy and goals surrounding the deal should be identified and a comprehensive valuation report prepared, focusing on key financials and tax returns over a substantial period of time, as well as organisational structure and shareholder agreements. This can help mitigate the risk that a company overpays in a transaction, even in the circumstance they are pressured to close the deal quickly.

Miscalculating or Overestimating Synergies

Consolidating two separate workforces and company cultures is a process that takes time and can accrue extra costs if expectations of integration are overestimated from the outset. Often, problems arise where a company is unrealistic about realising synergies, or the way in which two companies can function and operate more valuably together than they did individually.

Being conservative and focused on synergy estimates is one of the most important aspects of realising effective synergies. Attempting to generate synergies in every aspect of the business from the outset will likely lead to no synergies being realised at all.

Miscalculating synergies can also contribute to overpayment, where the synergies are calculated in the overall purchase price, and yet, the purchasing company does not receive the benefit of these synergies for a very long period of time.

An early focus on capturing the easiest synergies that will yield the highest return is perhaps the most advantageous way to approach synergies. Ensuring that stakeholders and team members are aligned around the overarching goal of the transaction can help guarantee that the correct synergies are captured to achieve this objective.

Integration Shortfalls

In the majority of M&A transactions the post-merger integration is actually the most complex and challenging part for the businesses. Post-transaction, both companies undergo major organisational changes to how they previously operated. This can oftentimes be a slow, tedious process, and is likely to fail without careful and considered planning prior to the initial stages of the transaction itself. Companies should ensure to prepare a detailed integration plan from the outset of the entire M&A process.

A comprehensive integration plan is integral to a successful post-transaction transition and should include addressing any potential challenges that may arise due the merging of the two different company cultures. Integration planning should begin very early, and businesses need to take into account the values, norms and assumptions of each individual company. This is not always an easy process, as the culture of a company can be difficult to identify. However, processes such as on-site visits, analysis of management styles and workflows and one-on-one conversations with employees can assist in ensuring that the companies are a cultural fit and provide a smooth integration process.

M&A Transactions in Thailand

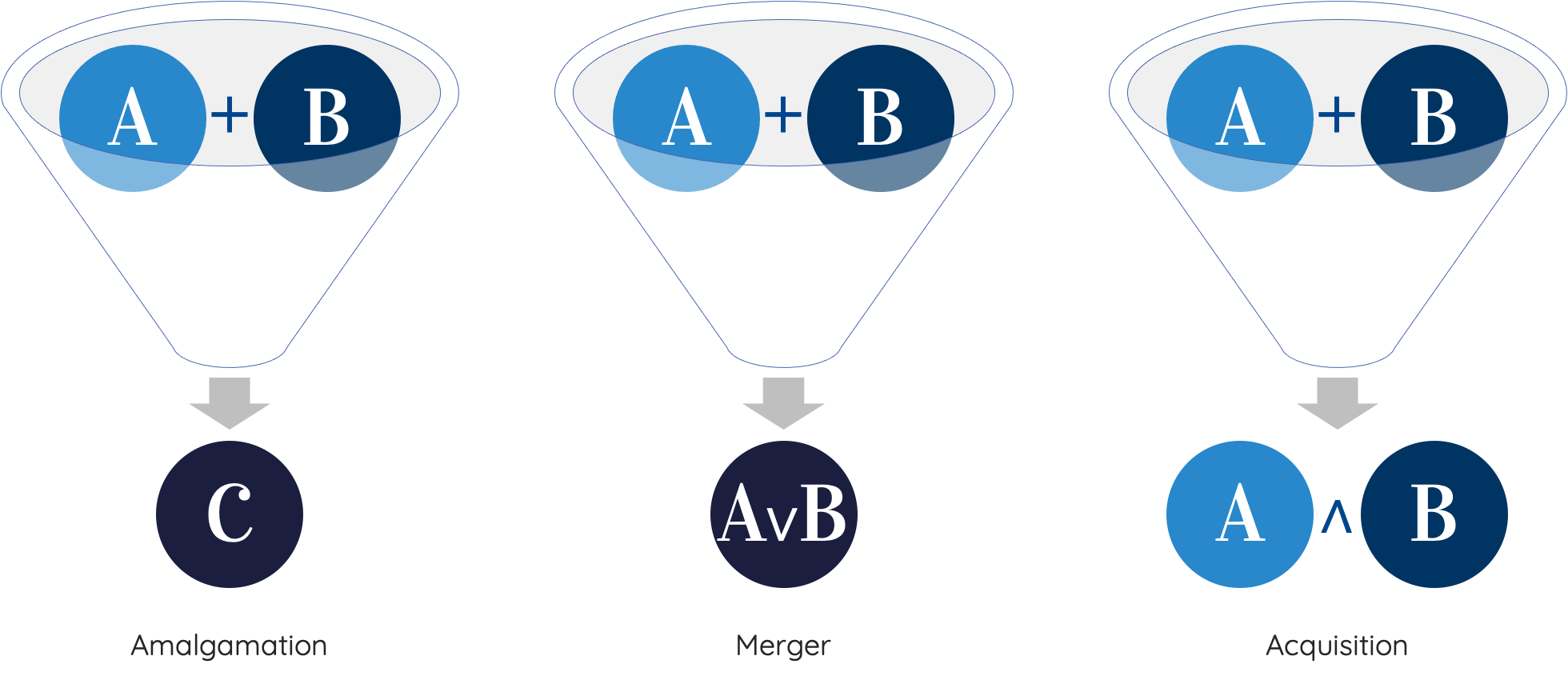

Currently, the Civil and Commercial Code (“CCC”) only recognizes the concept of “amalgamation” of companies, which refers to a transaction consummated by two or more companies to form a new company (A + B = C). Upon registration, the new company comes into existence, and the amalgamating companies are dissolved. The newly formed and registered company shall, by virtue of law, be entitled to all the property, obligations, rights, duties and responsibilities of the dissolved companies. Nonetheless, the transfer of business license to the new entity remains uncertain, in practice.

Recently, Thailand’s cabinet approved the draft amendment to the CCC (the “Proposed Amendment”) on 26 June 2020 and subsequently sent the same to the House of Representatives for parliamentary approval. The Proposed Amendment is to offer an alternative on a “merger” of companies, which refers to a transaction consummated by two companies (A + B), which are merged into a single company (either A or B). Where companies are merged, one of the merged companies (either A or B) will survive to succeed all the property, obligations, rights, duties and responsibilities of the dissolved companies.

Upon rechecking with the official at the Office of the Council of State, the House of Representatives has already resolved to accept the principle of the Proposed Amendment in Agenda 1 and is currently under consideration of the Commission of the House of Representatives before being officially promulgated in the Government Gazette.

With the Proposed Amendment, the amalgamation is no longer the only method for the combination of companies. Companies would have the alternative to undertake either a merger or an amalgamation, providing further that shareholders of each company cast vote of not less than three-fourths of the total number of votes of shareholders who attend the meeting and have the right to vote.

Figure 2. Amalgamations, Mergers and Acquisitions.

U.S. Tax Considerations

Due to FATCA, increased scrutiny from the IRS on international tax enforcement, and severe penalties, many people may be apprehensive about foreign investment or expansion. Although these issues must be addressed, some countries have blacklisted “tax havens,” where businesses can suffer tax consequences merely for conducting business in these countries. However, the IRS has no such rules. Rather, the U.S. has a set of anti-deferral rules and informational reporting for foreign investment. As long as these rules are met, there are no problems or penalties for foreign expansion.

The informational reporting is as straightforward as making sure all the correct forms are filed. For example, there is potential reporting for owning foreign bank accounts or owning foreign businesses. The anti-deferral regime, known in the U.S. as Subpart F, is a set of rules designed to tax businesses that appear to be operating in a foreign country merely to defer U.S. taxation. However, even if it is triggered, with proper planning the effects can be mitigated or even avoided completely. Worst case scenario is that the earnings are immediately taxed in the U.S., creating a virtual tax neutral situation that still allows expansion into Thailand at no tax cost.

Additionally, there are certain changes in U.S. tax law that may even make it easier for foreign expansion. While the rules might limit the ability to defer tax, they also may allow for more tax to be paid in Thailand and be credited on the U.S. return. This can be viewed as favorable in the local Thai community and create a good public opinion. Also, the participation exemption may allow for tax free repatriation of profits to a U.S. parent corporation. For these reasons it might be a better time than ever for entering the Thai market because not only are the new rules not harmful, but they may even be beneficial.

Overall, for most businesses there are no tax impediments to investing or expanding into Thailand, and, in some cases, there may even be benefits. Even if there are tax consequences, it is likely to create a tax neutral position rather than a cost or double tax. Furthermore, the reporting requirements are not to be feared if you are working with qualified professionals. Therefore, U.S. tax and reporting should not be viewed as a barrier to Thai investment or expansion — so long as appropriate measures and plans are in place.