Overview

Due to the unstable economic and health climate amidst the global pandemic, creditors and those interested in lending credit in Thailand have understandably been concerned about the repayment of debt owed to them. Fortunately for creditors, since the Debt Collection Act, B.E. 2558 (‘the Act’) entered into force in 2015, Thailand enjoys a rather comprehensive and effective debt recovery process including out of court settlements as well as litigation proceedings.

Key statistics

The importance of a straightforward debt collection process cannot be understated. Thai households are amongst the biggest borrowers in Southeast Asia, with approximations that up to 77.5% of Bangkok residents are in debt. Moreover, it is estimated that over half of those in debt are behind on their repayments and are at risk of default.

Now valued at 14.2 trillion baht, household debt is continuing to grow in Thailand, with a trend in which declining household income is prompting a rise in loans, thus creating more debt. The Debt Collection Act was established as a means to regulate how creditors collect debts and to offer increased protection and rights to individual debtors by banning amoral collection tactics.

Although the Act proved to be effective in the years following its enactment, the COVID-19 outbreak has had a devastating effect on household debt-to-GDP ratio, which grew to 90.5%—the highest level in 18 years, according to the Bank of Thailand.

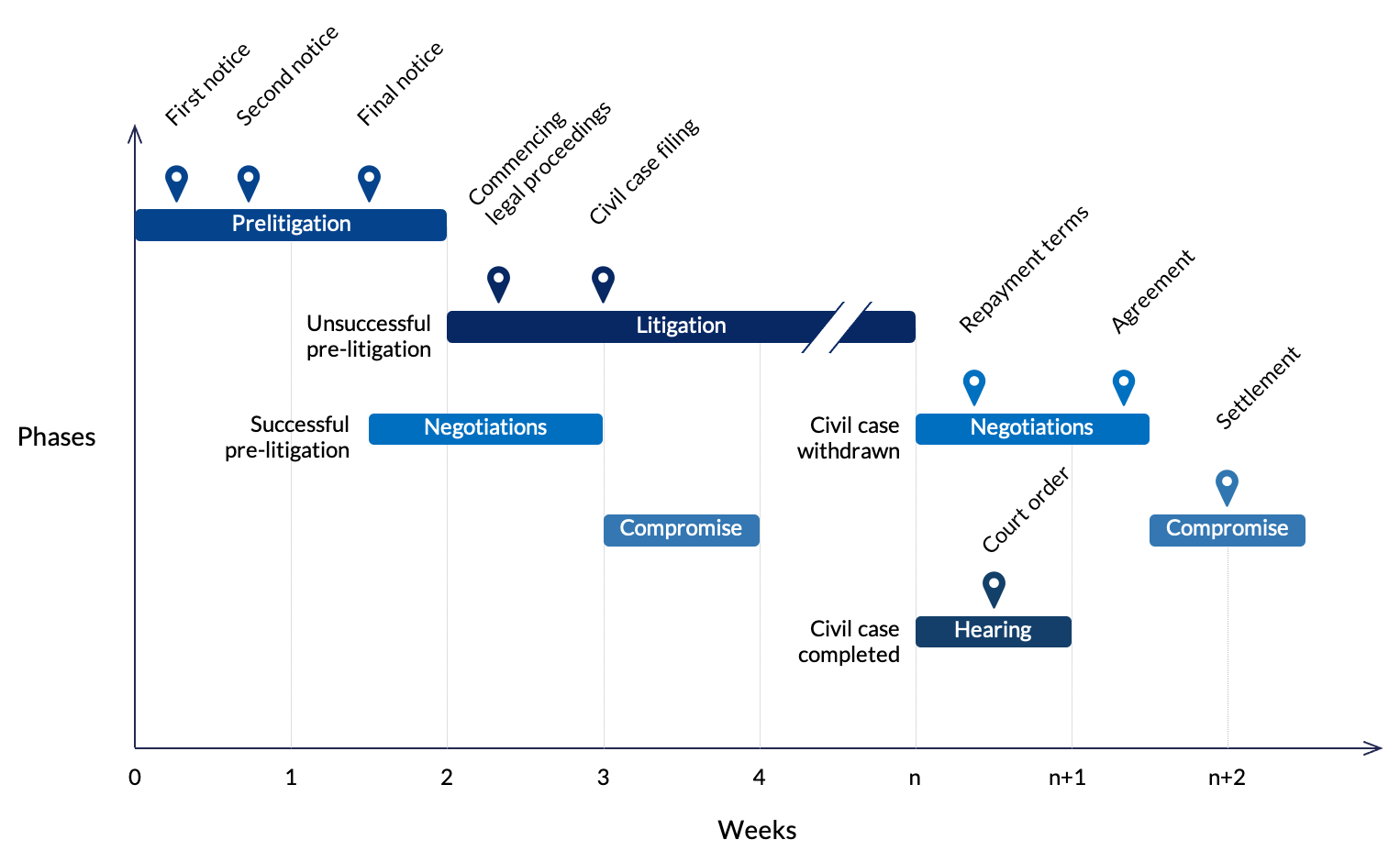

Stages of Debt Recovery

Debt collection in Thailand can be subdivided into two stages: pre-litigation and litigation.

Figure. Debt collection process.

Pre-litigation Debt Recovery

Creditors who have unsuccessfully attempted to recollect their accounts receivable through an in-house process may engage the services of a law firm with experience in debt recoveries. When debtors are unwilling to pay outstanding debts, lawyers are generally in a better position than creditors to secure a settlement with the obligor.

One of the main challenges in the pre-litigation phase is the difficulty of locating and contacting debtors, who may have changed their address. Sometimes, tracing a debtor may be a challenge, particularly in the event an insolvent company undergoes restructuring, rebranding, mergers or acquisitions, or even fraudulent bankruptcy. A capable debt collection professional would normally be able to identify the main obligors and guarantors, and to engage them so as to endeavour to swiftly reach an amicable settlement. The intended outcome of this phase is to bring the debtor to the negotiating table by means of demand letters, phone calls, or payment notices.

The pre-litigation debt recovery phase terminates with the occurrence of either of the following events:

Successful pre-litigation. Negotiations with the debtor are commenced, and a repayment schedule is agreed upon. The outcome of the negotiations is either a lump-sum repayment within a fixed deadline or instalment payments. Negotiations take on average between one week to 10 days.

Unsuccessful pre-litigation. When a debtor’s response is not forthcoming in the two-week pre-litigation phase, the creditor’s authorization will be sought to commence litigation proceedings. The threat of litigation issued as an incentive to bring the debtor to the negotiation table. If the debtor is willing to reach a settlement out of court, the plaint will be withdrawn.

Debt Collection Litigation

The litigation phase is much more complex than the pre-litigation stage, and it requires the creditor to retain the services of a law firm. In this phase, the law firm files a complaint in writing with the Court of First Instance. The written complaint outlines the nature of the claim, the relief sought and the allegation upon which the claim is based. When filing a complaint, it is important to consider some key factors, such as the merits of the claim, the designation of the case, the jurisdiction of the court, and the determination of relevant parties. When a civil case is filed in a Thai court, it is not uncommon for the judiciary to encourage the parties to settle the issue through a process of court- supervised mediation. A preliminary hearing is scheduled to identify any issues in the dispute and facilitate compromise between the parties. The court may also introduce a continuous trial, should it determine that a compromise is not likely to occur.

In the event of receiving an unsatisfactory judgment, the creditor may decide to appeal the decision to the Appeals Court. This must be done within a month of the date of judgement of the Court of First Instance. If there are significant questions of law, the appellant may apply to file an appeal to the Supreme Court of Thailand. A judgment of the Supreme Court of Thailand is final and binding upon the parties.

In the circumstance the claimant is successful, all the co-obligors are jointly and severally bound to pay the debt—inclusive of principal, interest, attorney’s fees and court fees incurred as a consequence of the debt—either in a lump-sum or in arrears.

The litigation phase ends with the occurrence of either of the following:

Civil case is withdrawn. If the debtor is responsive to negotiations, a repayment schedule is agreed upon and the case withdrawn. The outcome of the negotiations is either a lump- sum repayment within a fixed deadline or instalment payments. Negotiations take on average between one week to 10 days.

Civil case is completed. Once a judgment has been passed, the court allows one month from the time of the acknowledgement of judgment for the debtor to comply with the order. If the debtor chooses not to comply with the court’s order, an independent execution case is filed with the Execution Court.

Post-litigation

In the circumstance where the debtor has been ordered to repay their debt, but they fail to honour their payment obligations, the creditor is entitled to apply for an execution of the final judgment. The deadline for the execution is 10 years from the judgement pronouncement date. Should the debtor die, the creditor may seek repayment from the deceased’s estate, including life insurances, if any. Section 897 of Thailand’s Civil and Commercial Code stipulates that a creditor has the right to seek satisfaction from a deceased debtor’s insurance benefits when beneficiaries are unspecified. When beneficiaries are specified, creditors are only entitled to the amount of the premiums paid by the assured.

Dispute Resolution Methods

Four of the main methods to resolving disputes without the need for litigation are negotiation, mediation, collaborative practice, and arbitration.

1. Negotiation

Negotiations involve discussing issues in an effort to reach an amicable resolution. The role of a negotiator is to devise a feasible solution that suits the interests of both parties to a dispute. A settlement reached through negotiations is not binding upon the parties, unless they agree to enter into a legally binding compromise agreement, which contains a repayment schedule with an agreed-upon timeline for the reimbursement of principal amount plus interest.

2. Mediation

Mediation is an alternative dispute resolution method wherein a neutral third party assists the parties in dispute to find an equitable resolution. The mediator doesn’t represent either party and must unbiasedly facilitate the negotiations between creditor and debtor. Out-of-court mediation is accessible to any party in a relevant dispute and can be an effective mechanism for when the parties wish to maintain their relationship and protect their privacy, especially when it comes to sensitive financial information. Mediation is a viable method only if both parties are willing to reach a mutually acceptable compromise.

3. Collaborative Practice

Collaborative practices are another form of negotiation where the parties endeavour to reach a mutually acceptable settlement and agree to disclose relevant information in an attempt to avoid litigation.

In collaborative practices, each party is represented by their lawyer. The role of the lawyers is to minimize conflict, keep communications open and transparent, and achieve a fair solution. When handled professionally, collaborative practices may offer a more efficient, cost-effective, swifter, and private alternative to litigation in a court of law.

4. Arbitration

Arbitration is a form of dispute resolution that is generally less strict and more flexible than litigation. In arbitral proceedings, one or more arbitrators (customarily, one or three) are appointed, depending on the selected court of arbitration and on the decision of the parties. The parties are commonly represented by their lawyers who are invited to argue their case and present any relevant evidence. Arbitrators are ordinarily lawyers since they are experienced in different types of disputes and may be experts on the subject at hand. Arbitral awards are final and binding unless the parties agree otherwise in writing. Additionally, the parties may also agree to ad hoc arbitration, where the procedure may be determined independently of an arbitral tribunal. The International Chamber of Commerce rules and the UNCITRAL Arbitration Rules are two sets of comprehensive procedural rules which are commonly used for the conduct of ad hoc proceedings.

To request more information on MPG debt collection services, please address your request to our Litigation Department at [email protected].