Overview of the Insurance Industry

The insurance industry consists of companies offering risk management, by way of insurance contracts, to parties who pay a premium in exchange for guaranteed payment in the case of an uncertain future event. Insurance law governs all issues surrounding the practice of insurance. In particular, important aspects of insurance law include the regulation of business insurance, insurance policies, and the handling of claims. The insurance industry can be complicated and obscure, particularly for insured parties entering the industry for the first time. As such, it is vital that individuals and companies entering into insurance contracts be fully informed of the options available to them in the insurance sector, as well as their rights and obligations as a policyholder under a contract.

The Insurance Industry in Thailand

The Thailand insurance industry is vast, totaling in gross premiums of 285.6 billion Thai baht. The sector is primarily divided into two categories:

1. Life insurance; and

2. Non-life insurance (also known as general insurance).

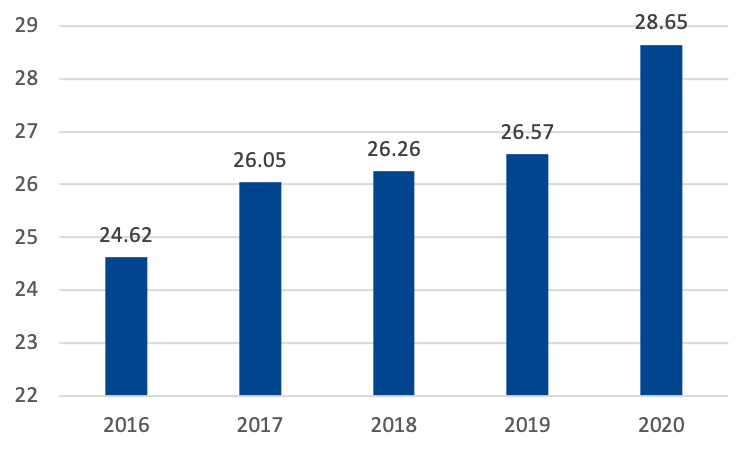

In 2020, the number of life insurance policies in Thailand went up to a total of 28.65 million from 26.57 million in 2019. Life insurance policies basically ensure that in the event of the insured’s death, the family will obtain monetary benefits, as well as other interests including wealth transfer, estate planning, estate tax liquidity and cash accumulation. Life insurance can be broken into two branches; term life insurance and permanent life insurance. Essentially, term life insurance provides coverage for a specific period of time and only pays the benefit if the insured dies during that specified time. Typically term life insurance is less expensive than permanent life insurance, which offers insurance for the insured’s entire lifetime, provided the premiums are paid in accordance with the insurance contract.

Figure 1. Number of Life Insurance Policies (in millions of Thai baht)

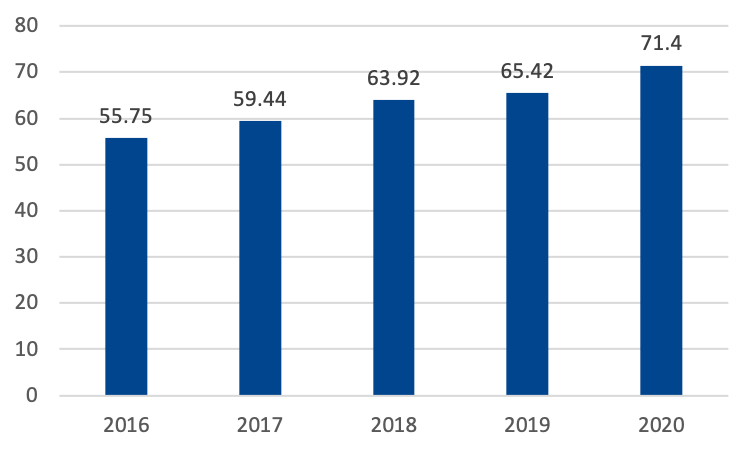

On the other hand, non-life insurance had a total of 71.4 million policies in 2020. Non-life insurance includes all other aspects of insurance such as auto insurance, property insurance, accident insurance, travel insurance, credit insurance, health insurance, personal injury and medical insurance.

Figure 2. Number of Non-Life Insurance Policies (in millions of Thai baht)

The Effect of COVID-19

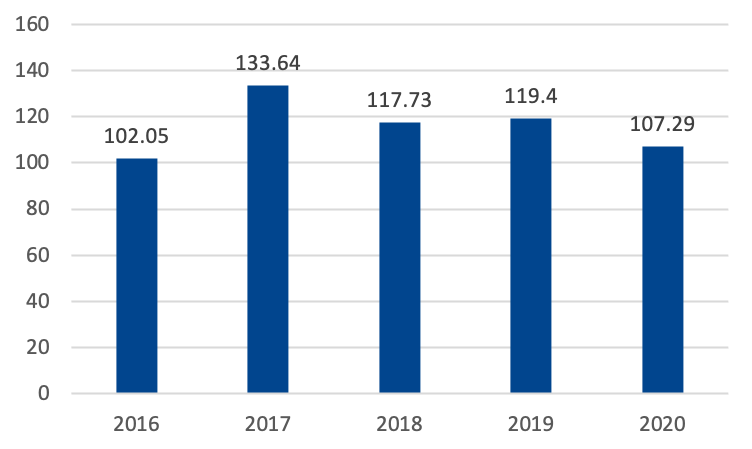

In general, Thailand’s insurance industry has been steady and growing throughout the 21st century. However this general trend does not translate to the non-life insurance industry. The total value of claims paid in 2020 took a sizable dip compared to the previous two years. This is particularly interesting as the total number of policies in 2020 was actually substantially higher than in previous years. Consequently, there are two conclusions that may be drawn; either policyholders are taking out less expensive insurance policies, which are likely to cover less, or, in a period of an increased need for claims and in an effort to save money, insurance claims are not being paid as regularly as in the past.

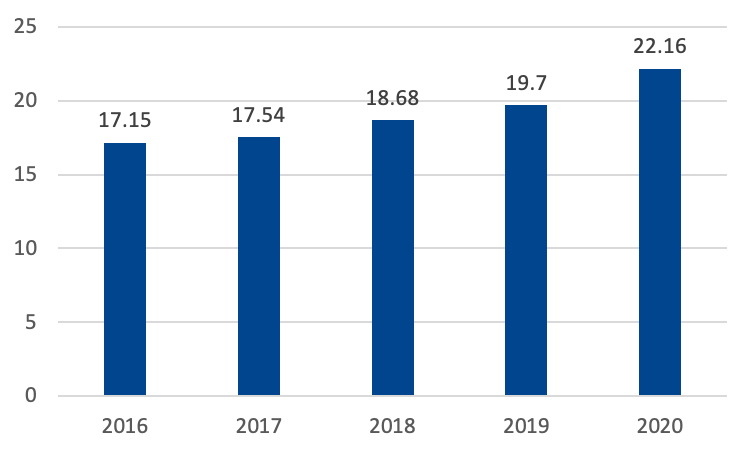

Figure 3. Value of Life Insurance Claims (in millions of Thai baht)

Conversely, the life insurance industry has been growing steadily each year. In fact it took its biggest leap forward in 2020, with the highest number of policies (and the biggest year to year increase) as well as the highest value of total claims paid. It is likely that this can be attributed to COVID-19 and the increased awareness of the necessity of life insurance, during a pandemic with a large number of people becoming ill and a high mortality rate.

Figure 4. Value of Non-Life Insurance Claims (in millions of Thai baht)

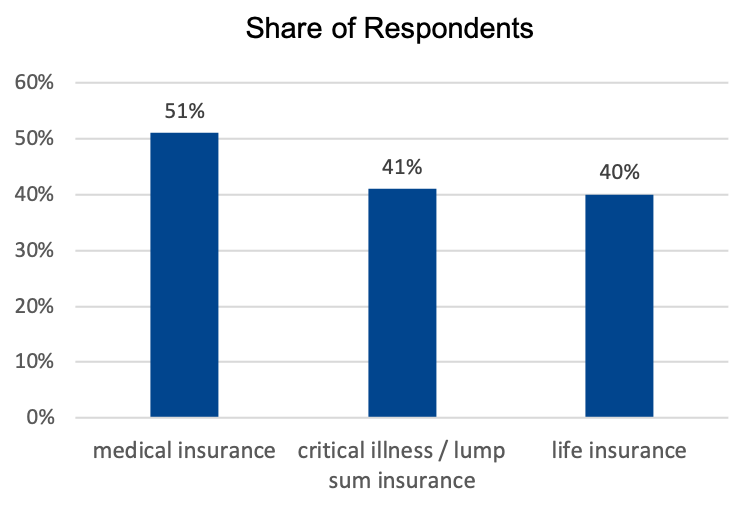

Customer behavior during the pandemic and the general effect of COVID-19 on the insurance industry can be analyzed by ascertaining what customers identified as their priorities during 2020. Unsurprisingly, 51% of respondents identified medical insurance as one of their top insurance priorities. This was followed by critical illness/lump sum insurance (41%) and life insurance (40%). The trend in priorities is likely based on the current threat of COVID-19.

Figure 5. Consumers’ insurance priorities after COVID-19 in Southeast Asia in 2020, by product type

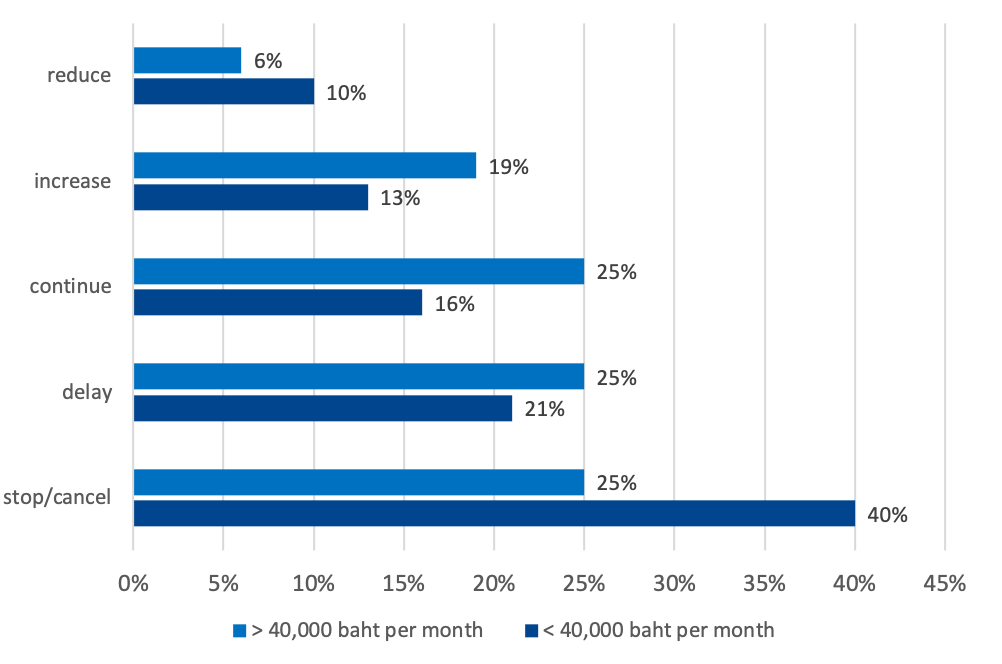

Notably, customer’s insurance needs and priorities differed depending on their respective income levels. Customers who earned less than 40,000 Thai baht per month were considerably more likely to stop or cancel their insurance policies compared to those over the 40,000 baht per month threshold. Further, customers earning under 40,000 Thai baht per month were more likely to cancel or stop their policy compared with any other cause of action such as delaying, continuing or reducing the policy.

On the other hand, the results from customers earning over 40,000 Thai baht per month indicated that that group were equally likely to cancel, delay, or continue their insurance policies, and they were much more likely to increase or continue their policies than those earning under 40,000 baht. Of course, this is not wholly unexpected, with the pandemic highlighting the difficulties of those in lower economic factions who have been forced to spend the majority of their income on bare essentials such as food and shelter, rather than having disposable income for insurance and investment. This is particularly worrisome as, generally, those in the lower income bracket have less capital to be able to afford expensive medical treatment in the event of an unexpected illness.

Figure 6. Impact of coronavirus (COVID-19) pandemic on consumers’ purchase intent for investment and insurance in Thailand as of March 2020, by income

Governing Insurance Body

The governing body of the insurance industry in Thailand is the Office of Insurance Commission (OIC), which regulates all insurance, reinsurance and all related business activities by insurer and reinsurance companies, and reports to the Ministry of Finance.

The organization was set up in 2007 via the Office of Insurance Act B.E. 2550 (“A.D. 2007”) (“OIC Act”). Unlike its predecessor, the Insurance Department, the OIC is not considered a government body, but an independent government agency. As such, it can be regulated and there are laws in place that restrict its powers and activities.

Relevant Insurance Laws and Regulations

There are a number of laws and regulations that govern the application of insurance issues in Thailand. The OIC has categorised acts and regulations affecting the insurance industry into three distinct categories:

1. Life Insurance

✓ Life Insurance Act B.E. 2535 (Amended by Life Insurance Act (No. 2) B.E. 2551 and (No. 3) B.E. 2558)

✓ Life Insurance Act No.2 B.E. 2553 (Amended B.E. 2551)

✓ Regulation under Life Insurance Act

✓ Life Insurance Act B.E. 2535

2. Non-Life Insurance

✓ Non-Life Insurance Act B.E. 2535 (Amended by Non-Life Insurance Act (No. 2) B.E. 2551 and (No. 3) B.E. 2558)

✓ Regulation under Non-Life Insurance Act

✓ Non-life Insurance Act B.E. 2535 (Amended B.E. 2551)

✓ Non-life Insurance Act B.E. 2535

3. Motor Insurance

✓ Motor Vehicle Victims Act B.E.2535 (1992)

Excluded Items and Refusal of Claims

The COVID-19 pandemic has emphasized the importance of insurance, particularly that of health insurance. Of course, in the midst of a global pandemic, having a financial safety net in the event of a COVID-19 infection is invaluable, taking into consideration the high cost of medical treatment without any insurance. The most prevalent insurance category during 2020 and 2021 has been health, however in a pre and post pandemic world priorities for different types of insurances are vast and ever-changing.

A large aspect of the insurance business model is to collect regular premiums, with the hope and expectation that a claim will not be made. On top of this, common medical procedures are regularly not included in standard insurance policies and insurance companies often require additional payments for such coverage.

The most commonly excluded items in health plans are:

✓ Pre-existing conditions

✓ Behavioral and personality disorders

✓ Fertility treatment

✓ Sleep disorders

✓ Specific scenarios listed in most health plans as exclusions

✓ Cosmetic or elective procedures

✓ Obesity

✓ Acquisition of an organ

✓ Off-label prescriptions

✓ Brand new technologies or products

Unfortunately, the insurance industry has a reputation of being somewhat volatile and insurance companies often deny claims brought forward by policyholders. If a claim is denied, policyholders are regularly given the option of purchasing additional coverage for an extra expense. Alternatively, denied claimants can appeal the decision to the insurance company who will review the decision and may end up accepting the claim, or correcting any mistake if applicable. In saying this, it is not in the interest of the insurance company to uphold an appeal and appeals are more often than not unsuccessful. For this reason, many claimants turn to the legal system to resolve disputes regarding denied claims with their insurance companies.

Dispute Resolution

In the event that an insurance company denies a policyholder’s claim, the aggrieved party may wish to resolve the dispute through dispute resolution. In Thailand, there are three key methods of dispute resolution available to those wishing to obtain a legal conclusion regarding their insurance dispute. These include:

1. Litigation

2. Arbitration

3. Mediation

Within the insurance industry all three mechanisms are regularly used to resolve disagreements and disputes between parties, each with their own advantages, disadvantages and processes. Importantly, having three distinct options for dispute resolution allows contracting parties to opt for a dispute resolution mechanism which best suits their needs and concerns.

Litigation

Litigation is the process of settling a dispute between two or more parties in a court of law. Essentially, litigation is a contested action, where one party brings a claim against the other who denies said claim. Unless the dispute can be settled before trial, a judge will generally make a final determination on the dispute.

The first step of any litigation is determining the jurisdiction of the matter. The Thailand Civil Procedural Code (CPC) regulates how jurisdiction is determined. The CPC sets out that the appropriate court to hear the dispute will be in Thailand where:

✓ The defendant is domiciled in Thailand;

✓ The plaintiff is domiciled in Thailand or is of Thai nationality;

✓ The defendant owns property in Thailand; or

✓ The cause of action arises in Thailand.

Determining jurisdiction is extremely important, particularly for the insured. Often, if there is a question as to jurisdiction, the insurance company may claim that they are not liable and cannot be forced to pay out the claim under that particular court.

Once the location has been selected for the jurisdiction, the value of the claim will determine if it will be heard in a provincial or district court. Determining the correct court is also an essential step. Different courts have the ability to deliver different judgement amounts. As such, it is crucial the right court is selected so the entirety of the claim can be enforced, and not just a portion of it.

Insurance claims in Thailand are classified as consumer cases under the Consumer Protection Act (CPA) and Consumer Case Procedure Act (CCPA). Thus, those bringing insurance claims to the courts are afforded the full benefits enjoyed by any customer bringing a legal action against a business. Individuals bringing an insurance claim enjoy immunity from court fees. Moreover, in line with a recent Supreme Court decision, the Court held that insurance policy clauses should be read in favour of the insured, which helps reduce the discernible power imbalance that exists between an insured and an insurer.

However, these benefits are not afforded to the insured where it is a business or corporation and the matter is treated as a normal civil suit. As such, the claimant will be subject to the usual court fees of between 0.1% to 2%, depending on the total size of the claim. The rationale for this is that businesses have more resources to pay for lawyers and court fees as compared to an individual.

Another key difference between insurance civil cases (brought by a business or corporation) and individual insurance consumer cases is that the CPC does not force disclosure by either party in insurance civil cases. Therefore, if a company is bringing a claim against an insurance company, they are not obliged to turn over any information they don’t want to. Where the insured is an individual, the CPAA allows the court to use its discretion to summon any witness or document to prove an issue.

While litigation is the most well-known mechanism for resolving disputes, it certainly has its downfalls. Not only is it often a lengthy process but it can be extremely cost invasive for both parties. The length of litigation can vary depending on the complexity of the case and whether or not it is appealed. Generally, an insurance case will take around a year to finalise from start to finish in the First Court, whereas if the matter reaches the Supreme Court it may take up to five years to reach a final verdict. This is particularly relevant to insurance claims, where claimants are often in immediate need of funds to cover the unexpected event that they need insured. Where an insurance claim is denied, if a resolution is not found quickly, it can have a serious impact on the financial situation of the insured, and in the worst-case scenario, result in bankruptcy. For this reason, the decision to litigate a matter should only be done after careful consideration, and with independent legal advice.

Arbitration

In an arbitration proceeding, the dispute is brought before an impartial third party known as an arbitrator, who makes a decision on the dispute after hearing evidence and arguments from both parties. The arbitrator will make their decision, also known as an ‘award,’ based on the merits of the case, and the decision will be binding on all parties involved in the dispute.

Generally, arbitration is a quicker and less expensive alternative to litigation, allowing individuals who would otherwise be deterred from the high costs of litigation to dispute their claim in a legal setting. On top of this, arbitration tends to be less confrontational than the traditional curial setting, and those unfamiliar with legal processes may feel more at ease bringing a claim through arbitration.

Arbitration is widely used in relation to insurance disputes in Thailand. Since 2008, the OIC has mandated that all insurance providers permit insurance contracts to contain a provision which allows the insured to decide whether they wish to use arbitration or litigation in the event of a dispute. Before appointing an arbitrator, it is common that parties attempt mediation to settle the dispute. If parties are still unable to reach an agreement, the OIC or related arbitration institution will schedule a meeting to appoint the appropriate arbitrators. Arbitral proceedings regarding insurance matters are conducted by an officer of the OIC. During the arbitration process, the insurer will be required to submit a defence as well as any details or supporting documents surrounding the claim.

Following the making of the award, parties are entitled to enforce or challenge the award under provisions of the Thai Arbitration Act. Typically, a decision arising from arbitration is enforceable by a court of law, and for the most part these decisions are not appealable. However, a short list of exceptions allows some circumstances in which an award can be appealed.

Possible reasons for appeal include:

✓ Lack of legal capacity of a party to the arbitration

✓ Ineffectiveness of the arbitration agreement under the law of the country agreed upon by parties as the governing law

✓ Service of process is not duly served on a losing party concerning the appointment of the arbitral tribunal or the arbitral proceedings

✓ An award is rendered outside the scope of the arbitration agreement or of relief sought

✓ Composition of the arbitral tribunal or the arbitral proceedings is not in accordance with parties’ agreement or the law of the country in which an award is made

✓ An award has yet to become binding or has been revoked or suspended by the competent court of jurisdiction or under the law of the country in which an award is made

Mediation

Mediation is generally quite a flexible form of dispute resolution, it is aimed at achieving a negotiated settlement. Mediation is less focused on determining the fault of either party, and instead, its objective is to assist parties in reaching a mutually acceptable agreement. Under this process, the mediator is an impartial third party who facilitates the negotiation between parties to reach a compromise and achieve settlement. Mediation is increasingly becoming the mechanism of choice for parties to amicably resolve their disputes. This is reflected in the CPA and CCPA, which state that courts have the discretion to order parties to mediate at any time prior to judgement, and mandate that courts direct parties to mediate prior to the initial hearing.

Insurance claims can be complex, involving intricate details related to legal issues. As such, mediators in the insurance industry are third party specialists, specifically trained to deal with various patterns of insurance disputes. Generally, mediation can be an attractive mechanism for the claimant of the insurance contract to resolve their dispute, as it is more efficient and less costly than other forms of dispute resolution. Accordingly, mediation assists the insured in facilitating their right to protection under the insurance policy as well as increasing the effectiveness of insurance claims management.

For the most part, mediation is used for non-life insurance claims and is a common resolution tactic for auto insurance and personal injury insurance claims. However, mediation can be a useful resolution mechanism for all insurance claims, including life insurance.

Concluding Comments

The insurance industry is an integral service for individuals and companies to protect themselves against unexpected events. The COVID-19 pandemic has emphasized the importance of insuring oneself against unforeseen circumstances and having a solid understanding of any such insurance coverage. Policyholders should ensure that they are educated on the best insurance contract to suit their needs. A useful way of having a holistic understanding of the most appropriate insurance contract is through detailed and thorough market research of available insurance policies and their coverage.

In the event a claim arises, it is the nature of the insurance industry that the policyholder may face difficulties in receiving payment from their insurance company. As such, it is not only important to ensure that the contract itself is iron clad, but that insured parties are aware of their options regarding dispute resolution. The process of getting a denied insurance claim honored can be difficult and lengthy, and insurance law is notoriously complex and detailed. It is essential that claimants have a strong legal advocate by their side to assist them in recovering their claim.