Customs Department Announcement No. 81/2020

In order to facilitate the obligations of importers of goods relating to the requirement of a certificate of origin (Form E) for customs and duty benefits during the coronavirus (COVID-19) outbreak, the Director-General of the Customs Department had issued an announcement to be in effect until 30 September 2020 and repealed Customs Department Announcement No. 47/2020. MPG had published an earlier update on this subject (learn more).

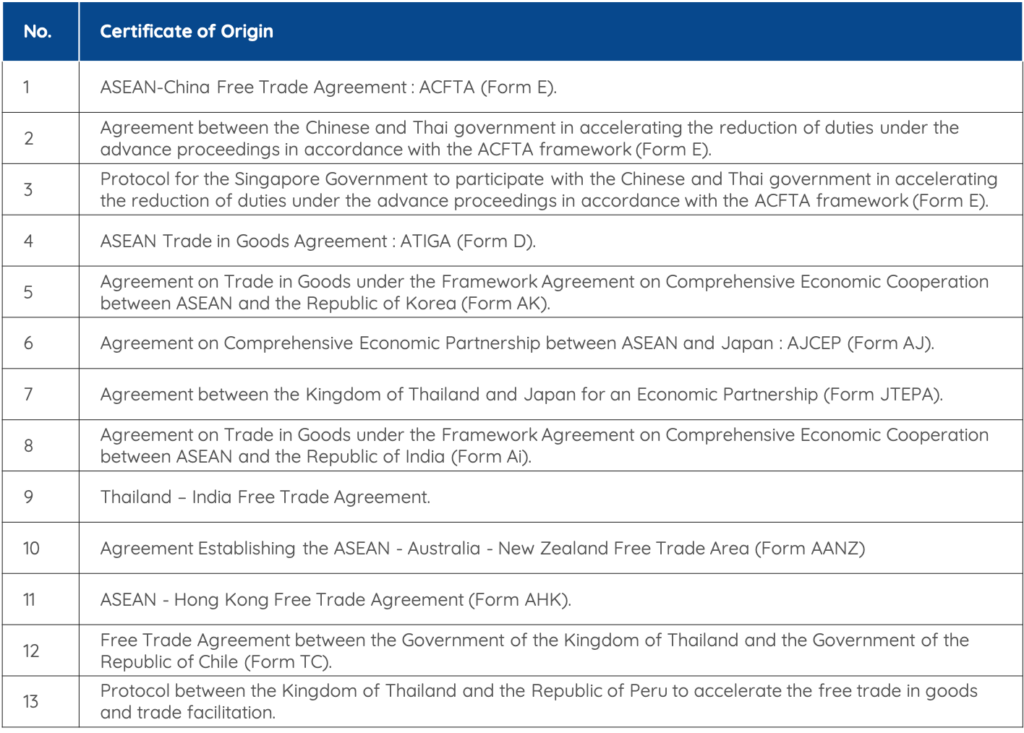

The new Announcement applies to the Free Trade Agreements that require importers to show the original certificate of origin when requesting customs and duties privileges.

Table 1: Types of Certificates of Origin

Importers are permitted to show a copy of the certificate of origin form where the importing country has already issued the form but cannot send the original certificate (as a result of its measures to control COVID-19) in order to proceed with customs clearance (article 3).

In order to be permitted to use a copy of the certificate of origin form for customs clearance, importers are required to do the following:

✓ Enter on the import entry form, in the Remark box: “ขอใช้สำเนาภาพถ่ายหนังสือรับรองถิ่นกำเนิดสินค้าไปพลางก่อนและจะยื่นต้นฉบับในภายหลัง” (which means “Request to use a copy of certificate of origin and the original certificate of origin will be submitted later”);

✓ Importers must meet directly with a Customs officer and must use the online system in order to request such meeting;

✓ Prior to retrieving the goods, the importer must submit for verification by the Customs Department, the form for permission to use the photocopy of the form, which may be accessed here.

✓ Within 30 days of customs clearance of the goods, the importer is required to submit the original version of the form to the Customs Department. If the importer does not make the submission within the prescribed time period due to the COVID-19 outbreak, the importer must submit a request 7 days prior to the deadline to extend the submission period, which must not be a total amount of 60 days. If the importer does not make the submission within the prescribed time period, duty exemptions and preferential tariff rates will not apply. An assessment will then be issued by the Customs Department for outstanding duties to be paid.

To request more information on MPG advisory services on Customs and International Trade, please address your request to [email protected].