On 19 January 2021, the Thai Revenue Department (RD) issued two notifications (Nos. 61 and 62) (“Notifications”) which extend the grace period for stamp duty payments on electronically executed instruments.

Payment of stamp duty is required when instruments are executed electronically for the following types of transactions (“Instruments”):

✓ Hire of work agreements;

✓ Loan agreements or bank overdraft agreements;

✓ Powers of attorney;

✓ Proxy letters for voting at company meetings; and

✓ Guarantee agreements.

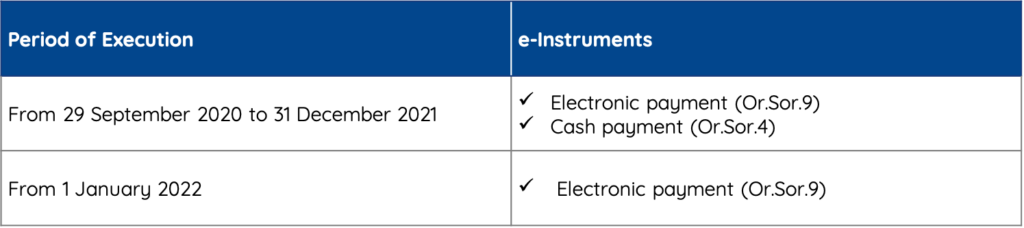

In 2019, the RD issued two notifications (Nos. 58 and 59) requiring parties to certain electronic transactions to pay stamp duty on an Instrument. To allow parties to adjust to the new payment method, a grace period was established until 31 December 2020. During this period, stamp duty payments on electronically executed Instruments (“e-Instruments”) could be submitted either electronically (form Or.Sor.9) or physically (form Or.Sor.4) to the Revenue Department. On 29 September 2020, the RD issued another notification (No. 60) permitting stamp duty on physically executed Instruments to be paid through the electronic system until 31 December 2020 as well.

Under the Notifications, the grace period for stamp duty payment methods is extended to 31 December 2021. Stamp duty on both e-Instruments and physical Instruments may be paid for either electronically or at the local Revenue Area Office. After the expiration of this period, all stamp duty payments on e-Instruments must be submitted electronically, while stamp duty on physical instruments must be paid at a Revenue Area Office.

Stamp duty must be paid within 15 days of an instrument’s execution. Late payments must be made in-person at a Revenue Area Office.