Summary

The rather outdated House and Land Tax Act B.E. 2475 promulgated in the 1930s has been recently replaced by a new Land and Building Tax Act B.E. 2562, which has come into force on 13 March 2019. This statute represents a landmark tax reform that imposes taxes on individuals or companies that own or have possessory, or usage rights to immovable assets (i.e. land and buildings, including condominiums) in Thailand. Under the previous regime, taxes were charged on earnings from renting or leasing out properties and not on the asset itself, essentially serving as an income tax rather than a property tax scheme. The new Land and Building Tax Act now gives local government authorities the right to collect taxes on land and buildings in Thailand. The objectives of the new Act are to make tax collection more efficient and to increase public revenue. Tax collection under the new Act will begin on 1 January 2020 and is to be paid in April each year. The value of the land and buildings will be appraised by the government, and the assessed price will serve as the basis for calculation of the property tax.

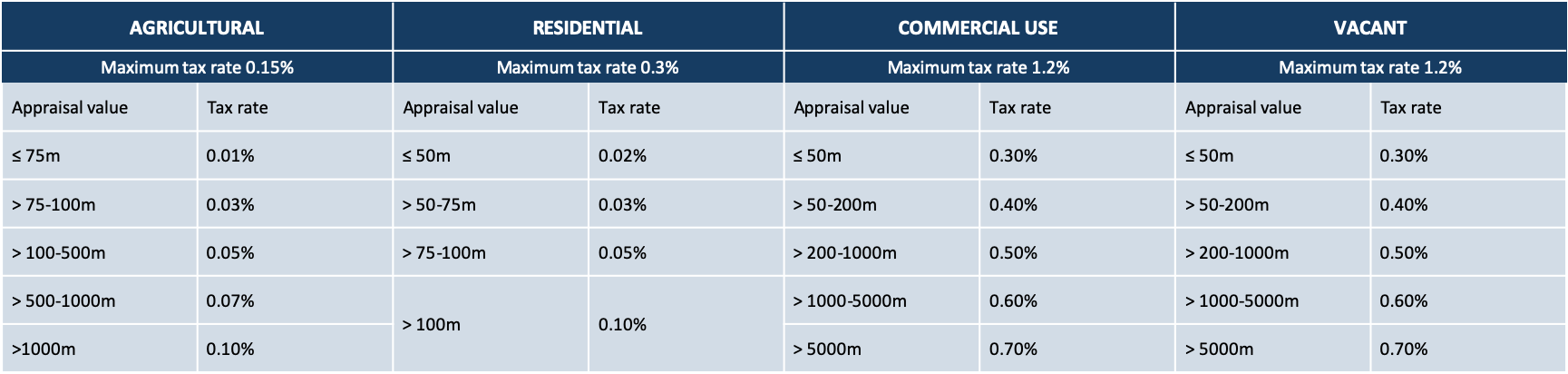

Transition Period Rates

For the first 2 years of tax collection starting from 1 January 2020, which is regarded as the transition period, a land or building owner will be liable for reduced tax rates as follows:

Also, an owner (individual/person) of land or a building that is used for agricultural purposes, will be exempt from tax for the first 3 years, starting 1 January 2020. The applicable tax rates from tax year 2022 onwards will be announced by way of royal decree. It is worth mentioning that the Act allows local collection agents to impose higher tax rates using local legislation, than the rates prescribed by royal decree. Nonetheless the rates imposed by local legislation cannot exceed the maximum rates outlined above. There is also a special clause for land and buildings that are unused for more than 3 consecutive years. The tax rate charged on the latter will increase by 0.3% every 3 years, until the rate reaches the cap of 3%.

Exemptions

The Act provides a number of exemptions from tax to an owner of the following:

✓ Land or a building that is worth up to THB 50m and used for agricultural purposes.

✓ Land or a building that is worth up to THB 50m and used for residential purposes, provided the owner’s name is on the house registration book as of January 1 of that year.

✓ A building (i.e. not land) that is worth up to THB 10m and used for residential purposes, provided the owner’s name is on the house registration book as of January 1 of that year.