I. Current Tax Collection Regime in Thailand

Thailand’s personal income tax system incorporates both territoriality and residency-based principles:

✓ Territoriality (Source-Based): Tax is imposed on all income generated within Thailand, regardless of the taxpayer’s residency status.

✓ Worldwide Income (Residency-Based): Residents must report foreign-sourced income if it is remitted into Thailand, regardless of the tax year in which it was earned.

Key concepts include:

✓ Accrual Basis: Income is recognized when the right to receive it arises, not necessarily when received.

✓ Remittance Basis: Foreign-sourced income is taxable only when brought into Thailand.

Under Section 41 of the Revenue Code, taxpayers must pay tax on income earned in Thailand, while residents earning foreign-sourced income must report it when brought into Thailand. Individuals are considered residents for tax purposes if they stay in Thailand for at least 180 days in a tax year.

II. Recent Updates on Foreign-Sourced Income

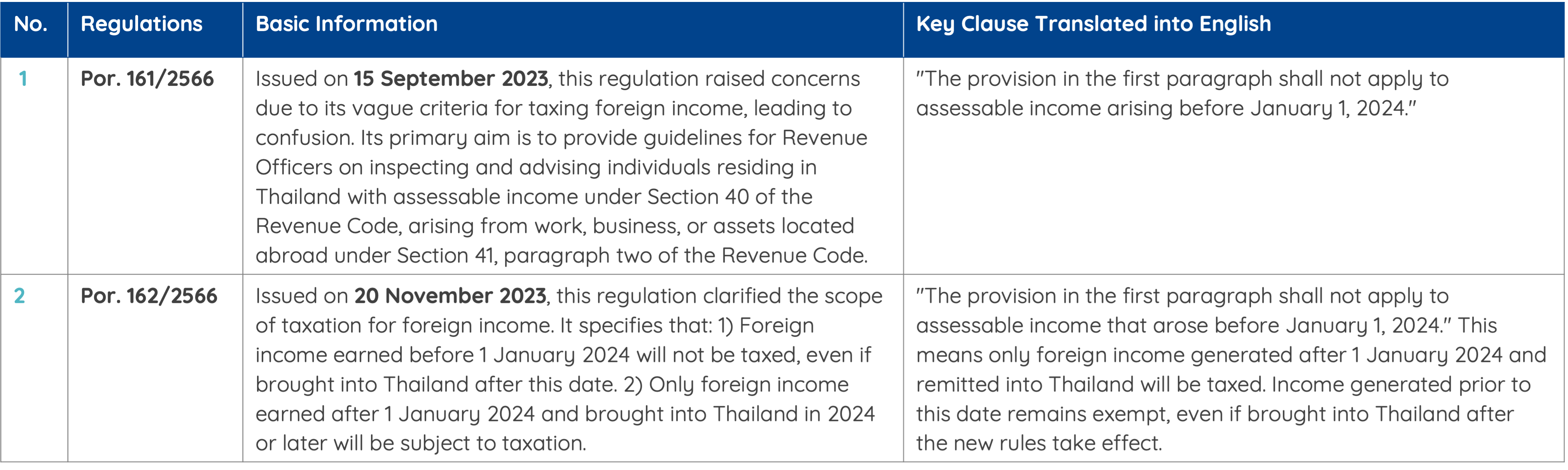

The Revenue Department issued Order No. Por. 161/2566 and No. Por. 162/2566, providing clarity on the taxation of foreign-sourced income:

✓ Por. 161/2566 (September 2023): Introduced guidelines for taxing foreign income but left ambiguity regarding income earned before 2024.

✓ Por. 162/2566 (November 2023): Clarified that foreign income earned before January 1, 2024, will not be taxed if brought into Thailand in 2024 or beyond. Only foreign income earned after January 1, 2024, and remitted into Thailand, will be taxed under Section 41 of the Revenue Code.

Conditions for Taxability:

1. Residency Requirement: The taxpayer must reside in Thailand for at least 180 days in the relevant tax year.

2. Income Remittance: Foreign income must be brought into Thailand within the tax year or later to be taxable.

These updates provide clarity and alleviate concerns about retroactive taxation.

Figure 1. Overview of Revenue Department Orders Por. 161/2566 and Por. 162/2566.

III. Tax Calculation Methods and Assessable Income Categories

Thailand employs two methods for calculating personal income tax, with taxpayers required to pay the higher of the two amounts:

1. Section 48(1): Tax is calculated based on assessable income, less exemptions, expenses, and deductions, then multiplied by the progressive tax rate. A = {[(Assessable income – Exempt income) – Expenses] – Deductions} × Income tax rate.

2. Section 48(2): Tax is calculated at a flat rate of 0.5% on the total assessable income derived from categories (2) through (8). B = (Assessable income (2) through (8) – Exempt income) × 0.5%.

Taxable Income Categories:

The assessable income is classified into eight categories:

1. Income from wages and salary, including the benefits provided by an employer (e.g., income from stock options, personal income tax paid and absorbed by the employer, living allowances, monetary value of rent-free accommodation, etc.), but excluding business travel expenses and medical treatment.

2. Income from employment or services rendered.

3. Income from royalties (goodwill, copyright, franchise, patents or other rights)

4. Income from dividends, interest (e.g., on deposits with banks in Thailand), capital gain, bonuses for investors, acquisition or dissolution of companies or partnerships, etc. However, this does not include the share of profits obtained from a non-juristic body of persons or from the sale of investment units in a mutual fund.

5. Income resulting from leasing out a property.

6. Income resulting from professional services (e.g., law, medicine, engineering, accounting, architecture and fine arts).

7. Income resulting from construction and other related contractual arrangements, whereby the contractor provides essential materials.

8. Income from business, commerce, agriculture, industry, transport or any other activity not-specified here above (carry-all clause). Insurance benefits, inheritances & scholarships, however, are not considered as assessable income and are thus not subject to personal income tax.

Currency conversion for foreign income follows the rates specified by the Exchange Control Act B.E. 2485.

IV. Tax Credits and Double Taxation Agreements (DTAs)

To mitigate double taxation, Thailand offers tax credits for foreign taxes paid, governed by DTAs established with 61 countries. Key provisions include:

✓ Tax credits are capped at the lesser of the foreign tax paid or the Thai tax due on the same income.

✓ Credits are calculated separately for each type of income.

Example: If a taxpayer earned 500,000 THB in foreign-sourced income, paid 75,000 THB in foreign taxes on this income, and the Thai tax liability on the same income is calculated as 50,000 THB, the allowable tax credit is capped at 50,000 THB, which fully offsets the Thai tax liability. The excess 25,000 THB in foreign tax paid cannot be credited or refunded under Thailand’s tax laws, as tax credits are limited to the lower of the foreign tax paid or the Thai tax liability.

Taxation Rights Under DTAs:

✓ Real Estate, Dividends, and Interest: Taxable by both residence and source countries.

✓ Business Profits: Taxable by both countries if there is a permanent establishment (PE); otherwise, taxed by the residence country.

✓ Employment Income and Pensions: Taxable by the residence country.

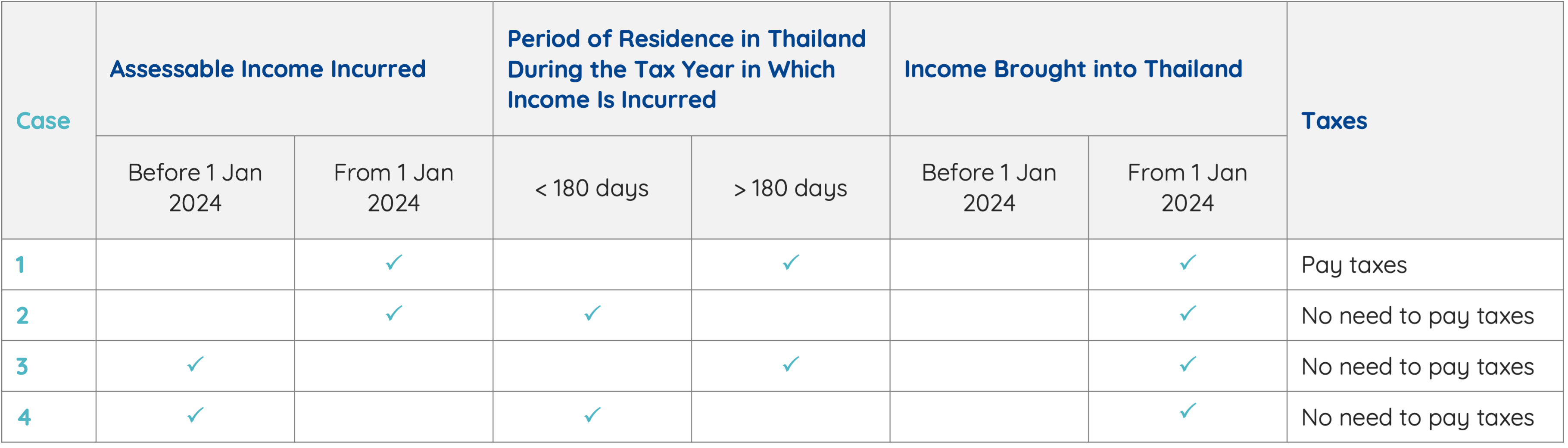

V. How These Changes Impact Taxpayers

From January 1, 2024, the updated rules clarify Thailand’s taxation of foreign-sourced income, providing certainty for residents earning income abroad. The inclusion of tax credits ensures that individuals are not doubly taxed, making Thailand’s system more aligned with international standards.

Figure 2. Summary of Tax Implications for Income Earners Bringing Income into Thailand.

Mahanakorn Partners Group (MPG) is well-positioned to assist individuals and businesses in navigating these changes, ensuring compliance with Thai tax laws while optimizing tax strategies. Whether you need guidance on foreign income reporting, tax credit calculations, or structuring your finances to minimize liabilities, MPG’s experts are here to help.