Customs Department Announcement No. 4/2020, May 22, 2020

The use of Invoice 2 for Customs clearance to receive tariff privileges under the Free Trade Agreement (FTA)

The Customs Department, Tariff Division has announced that importers ordering products through a company in Thailand are permitted to use a second invoice for customs clearance in order to receive tariff privileges under the Free Trade Agreement (FTA). The nature of this transaction is detailed in the attachment to this announcement.

Parties of eligible transactions can apply for tariff privileges under the FTA by submitting a second invoice (domestic trading) for Customs clearance and specifying the product price according to the domestic product price list in the Import Entry form. As these transactions are not considered to be third-country trade, a “/” mark is not required in the “Third Country Invoicing”, “Third Party Invoicing”, or “Subject of third-party invoicing” box in the Certificate of Origin, as the case may be.

Trade Transactions between FTA Signatory Countries

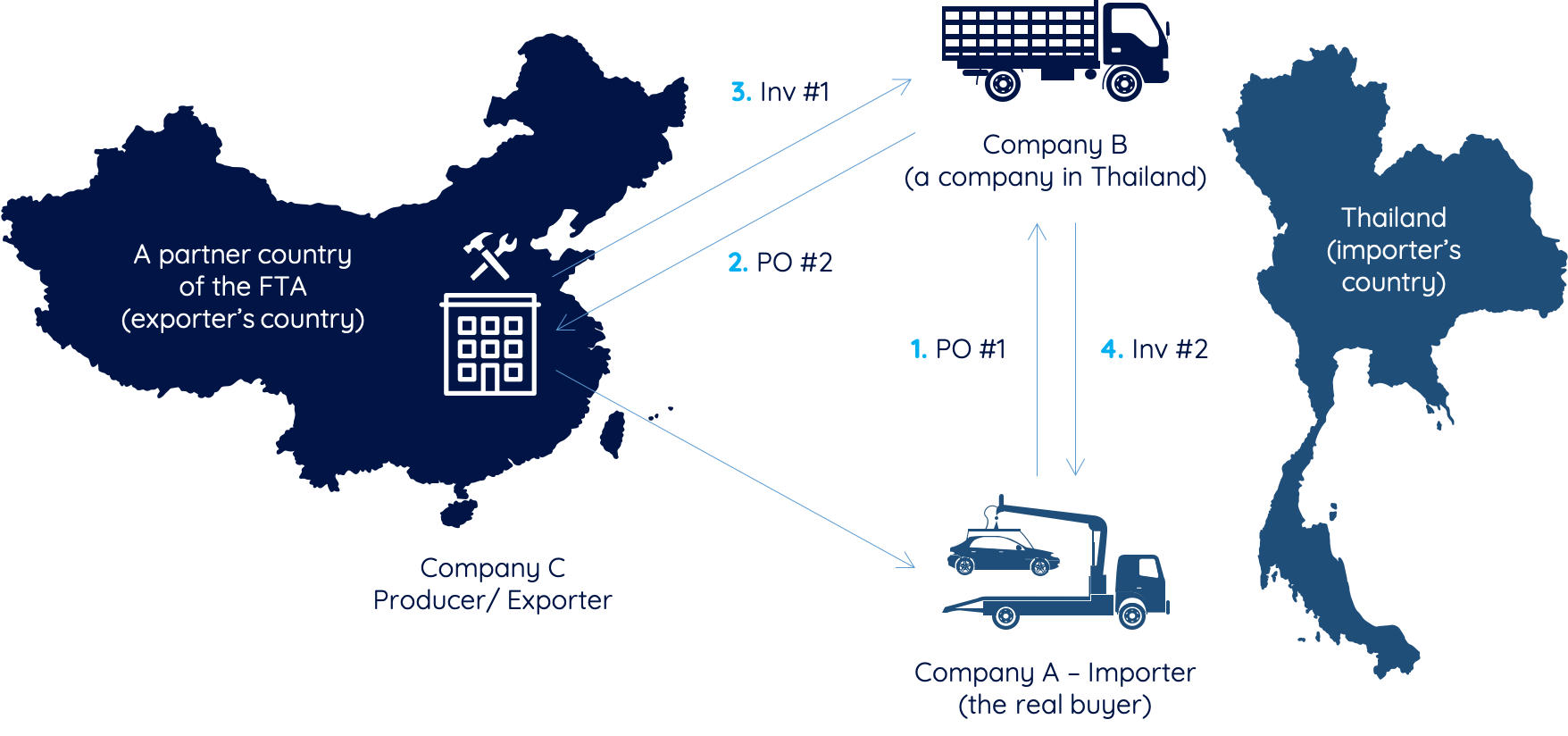

The characteristics of transactions in which the importer orders products through a company in Thailand, which submits a second invoice for customs clearance in order to receive customs privileges under the FTA, are illustrated in the following example:

The real buyer in Thailand, Company A, orders products through Company B, a company in Thailand. Company B will order products produced by Company C, a company in an FTA signatory country. Once Company C finishes manufacturing the products, Company C will ship the products to Thailand and issue a CO Form to receive tariff privileges. The exporter in the CO Form will be specified as Company C and the importer will be Company A, the real buyer in Thailand. Company C will issue an invoice to bill Company B (Invoice 1), and Company B will issue an invoice to Company A (Invoice 2).